4 Jun 2026

Credit card reward points look simple on the surface. You spend money, points get added, and later you redeem them for vouchers, cashback, flights, hotels or other benefits. For many people, it feels like a small bonus for using a card. But behind those points sits a larger economic system involving card issuers, merchants, payment networks, loyalty partners and consumer behaviour. This topic matters because credit card usage in India has grown sharply. According to the RBI’s Payment System Report, India has around Rs. 11.94 crore credit cards outstanding as of April 2026.

So, reward points are no longer a niche luxury feature. They are now part of everyday personal finance. Used well, they can reduce travel costs, improve value from regular spending and help people think more carefully about expenses. Used badly, they can encourage overspending, create debt and hide the real cost of “free” benefits.

Source: RBI, as per latest data available

What Exactly Are Reward Points?

Reward points are benefits earned when a cardholder uses a card for eligible transactions. RBI defines card loyalty or reward programmes as schemes where card issuers or associated merchants offer digital coupons, points, discounts, cashback or other benefits with monetary value, which can be used for the same transaction or future transactions. The important point here is: one reward point does not automatically mean one rupee. The value depends on how and where it is redeemed. Another reason the same number of points may create different value across merchants or spending categories is that the economics behind card transactions are not always identical. Merchant Category Codes (MCCs) classify businesses where cards are used and can affect merchant charges and reward treatment. RBI has also stressed transparency in MDR charges. Different MCCs may partly explain why the same points do not always have the same value, though issuer rules, partner arrangements, and redemption choices also play an important role.

Why Do Reward Points Exist?

Reward points exist because they influence behaviour. They encourage people to use one payment method more often, spend through formal digital channels, remain loyal to a card issuer and choose specific redemption partners. In the payment’s ecosystem, merchants usually pay a cost for accepting card payments. This cost is commonly linked to the Merchant Discount Rate, or MDR. RBI has specifically required merchant charges to be clearly unbundled for different categories of cards so that there is more transparency at the merchant level.

In practice, a part of the economics generated from card usage supports the reward system. Some rewards are funded by issuer economics, some by merchant partnerships, some by annual fees, some by marketing budgets, and some by loyalty partners who want access to high-spending customers. This does not mean every reward is “free money”. The cost is effectively built into the system. Broadly, credit card users fall into two groups: transactors, who pay their balance in full and avoid interest, and revolvers, who carry balances and pay interest. Issuers earn interest from revolvers, while transactors are monetised through merchant fees, annual charges, and partner arrangements. This helps explain why reward programmes can exist even for cardholders who never pay interest.

The Hidden Benefit: Converting Normal Spending into Future Value

The best way to understand reward points is to treat them as a small return on necessary spending, not as a reason to spend more. The value becomes meaningful only when the points are earned on expenses that would have happened anyway and redeemed in a category where the value per point is strong. If a person spends on groceries, fuel, bills, insurance, travel, education fees or shopping anyway, earning points on those payments can create incremental value.

For example, assume a person spends ₹50,000 per month on regular, necessary expenses through eligible card transactions. That is ₹6 lakh per year. If the effective reward value is only 1%, the value created is around ₹6,000. If the person redeems those points more efficiently and gets 2% equivalent value, the benefit becomes ₹12,000. This may not sound huge in one month. But across three to five years, the value can become meaningful. The missed value comes when people earn points but forget to redeem them, redeem them for low-value options, let them expire, or spend unnecessarily just to chase more points.

Source: ET article dated Mar 12, 2026

Why Flights And Hotels Can Significantly Reduce Out-Of-Pocket Costs

Travel is often where reward points can create the highest perceived value. This does not mean every flight or hotel can become free. It means that with smart planning, reward points can reduce the largest part of the cost. Airline and hotel loyalty systems are built around future redemption. IATA’s industry accounting guidance notes that airline loyalty miles can be issued through credit card usage and redeemed for travel or other services under loyalty programme terms.

Here is the simple logic. A flight ticket has multiple components: base fare, airline charges, taxes, airport fees and convenience costs. Reward points may cover the fare or a large part of the fare, but taxes, fees and surcharges may still have to be paid. IATA’s guidance also explains that passenger taxes and related fees collected on behalf of governments or airport authorities are separate from the airline’s own revenue. So, the right way to say it is points can make flights or hotels almost free, not always completely free.

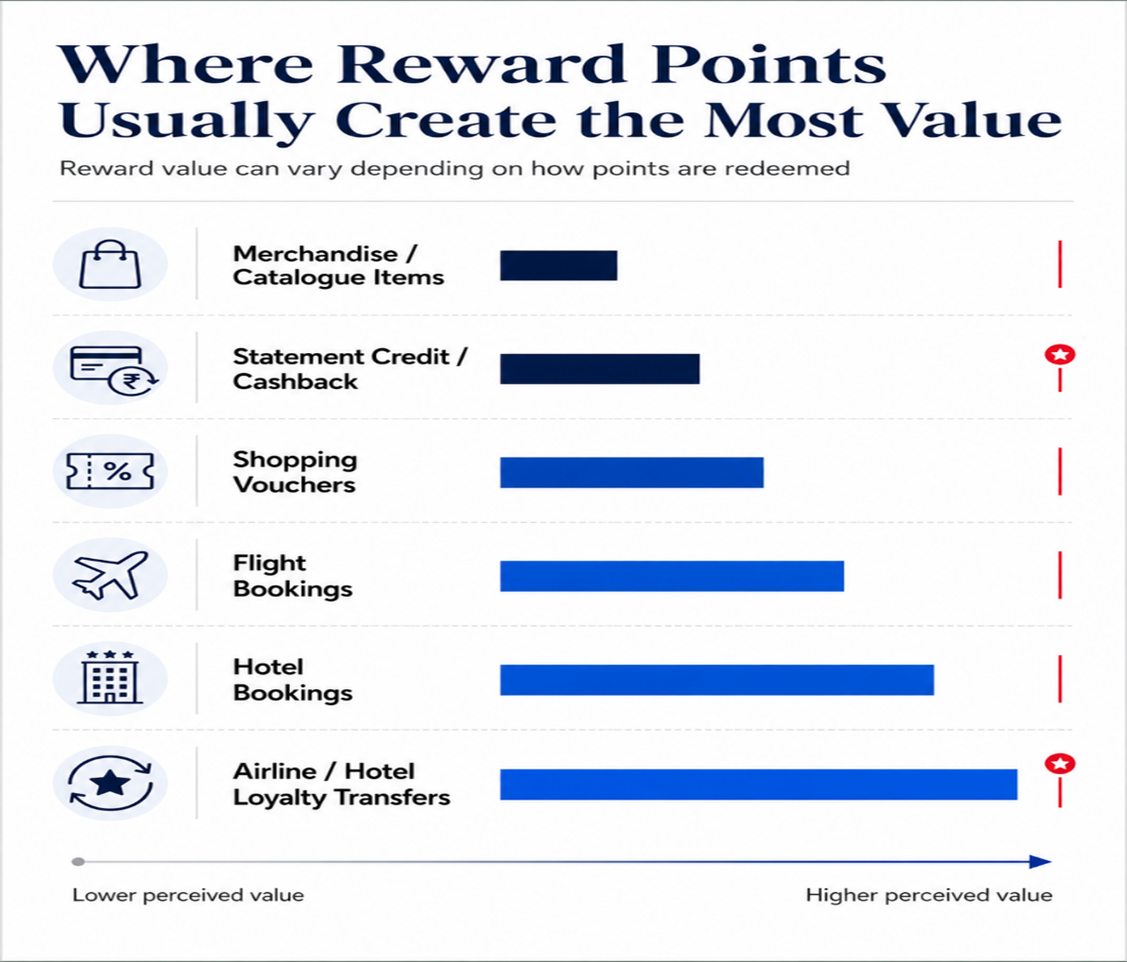

Where Can Reward Points Be Used?

Many people collect points but do not know where to use them, so they either let the points expire or redeem them for low-value options. Reward points can usually be used across multiple categories such as travel bookings, hotel loyalty programmes, airline loyalty programmes, shopping vouchers, gift vouchers, merchandise catalogues, statement credit or partner transfers. One key benefit of credit cards is that they convert everyday spending into rewards such as cashback, points, travel perks, discounts, and lounge access (subject to terms and conditions). These benefits are supported by issuers, merchants, loyalty partners, annual fees, and marketing budgets, creating strong value for disciplined users who pay on time and avoid interest costs.

For example, some cards may allow users to transfer reward points to hotel loyalty programmes. In such cases, the cardholder may convert credit card reward points into hotel points and use them for room bookings, upgrades or other hotel-related benefits, depending on the programme rules.

Similarly, points may also be used for flight bookings, where the user can reduce the cash amount paid for the ticket. However, it is important to remember that points may not always cover taxes, convenience fees, surcharges or other charges. Points can significantly reduce out-of-pocket costs, rather than saying that travel is always completely free.

A simple example can make this easier.

Assume a card gives 2 reward points for every ₹100 spent on eligible transactions.

| Monthly / One-Time Spend | Reward Rate | Points Earned |

|---|---|---|

| ₹1,00,000 | 2 points per ₹100 | 2,000 points |

Now the value of these 2,000 points will depend on where they are redeemed.

| Redemption Option | Illustrative Value Per Point | Approximate Value from 2,000 Points | Value Quality |

|---|---|---|---|

| Merchandise catalogue | ₹0.10–₹0.20 | ₹200–₹400 | Usually low |

| Gift vouchers | ₹0.20–₹0.30 | ₹400–₹600 | Moderate |

| Statement credit / cashback | ₹0.20–₹0.30 | ₹400–₹600 | Simple but not always highest |

| Flight booking | ₹0.30–₹0.50 or more | ₹600–₹1,000+ | Can be better |

| Hotel booking / hotel partner transfer | ₹0.50 or more in good cases | ₹1,000+ | Often attractive if planned well |

| Airline / hotel loyalty transfer | Depends on partner and availability | Can be higher than direct redemption | Potentially high, but variable |

This shows why the same 2,000 points can feel very different depending on the redemption method. If the user redeems them for a low-value catalogue product, the benefit may be small. But if the same points are used smartly for travel or hotel redemptions, the effective value may be much better.

Source: wishfin.com

How to calculate the real value of points

The most important habit is to calculate the value per point before redeeming.

Use this formula: Value per point = Cash price avoided ÷ Number of points used

If 10,000 points save ₹2,000, the value is ₹0.20 per point. If the same 10,000 points save ₹5,000 on a hotel or flight, the value is ₹0.50 per point. This is why blindly redeeming points for catalogue items can destroy value.

A good rule is simple: before redeeming, compare at least three options - cashback or statement credit, vouchers, and travel. The better option is not always travel. If a flight is cheap in cash, using points may be wasteful. If a hotel price is unusually high, points may be excellent.

Advantages Of Reward Points

Reward points transform regular spending into meaningful value - helping reduce travel, shopping and lifestyle expenses through cashback, vouchers and redemptions.

Used responsibly, credit cards can also become an efficient financial tool by offering an interest-free payment period when dues are paid in full and on time.

Beyond savings, reward points can unlock premium travel experiences such as flight upgrades, better hotel stays and exclusive benefits, adding lifestyle value without significantly increasing cash outflow.

Disadvantages And Risks

The biggest risk is debt. Reward points are never worth paying with credit card interest, which can often range between 30% and 45% annually if dues are not paid on time. If a user pays only the minimum amount due, the benefit of points can disappear very quickly. RBI requires card issuers to warn customers that paying only the minimum amount every month can stretch repayment over months or years with compounded interest. RBI also states that the interest-free period is suspended if any previous month’s balance remains outstanding.

The second risk is overspending. Many people justify unnecessary purchases by saying, “I will earn points.” That is a trap. Spending ₹10,000 extra to earn points worth ₹100 or ₹300 is not smart finance.

The third risk is devaluation. Points can lose value if redemption rules change, conversion ratios are revised, caps are introduced, or certain categories stop earning rewards.

The fourth risk is poor redemption. Merchandise catalogues, low-value vouchers or unnecessary products may give very low value per point. The customer feels rewarded, but the actual financial value may be weak.

The fifth risk is availability. Flights and hotels booked through points may be subject to seat availability, blackout dates, limited inventory or dynamic pricing. Thus, points work best for people who plan early and stay flexible.

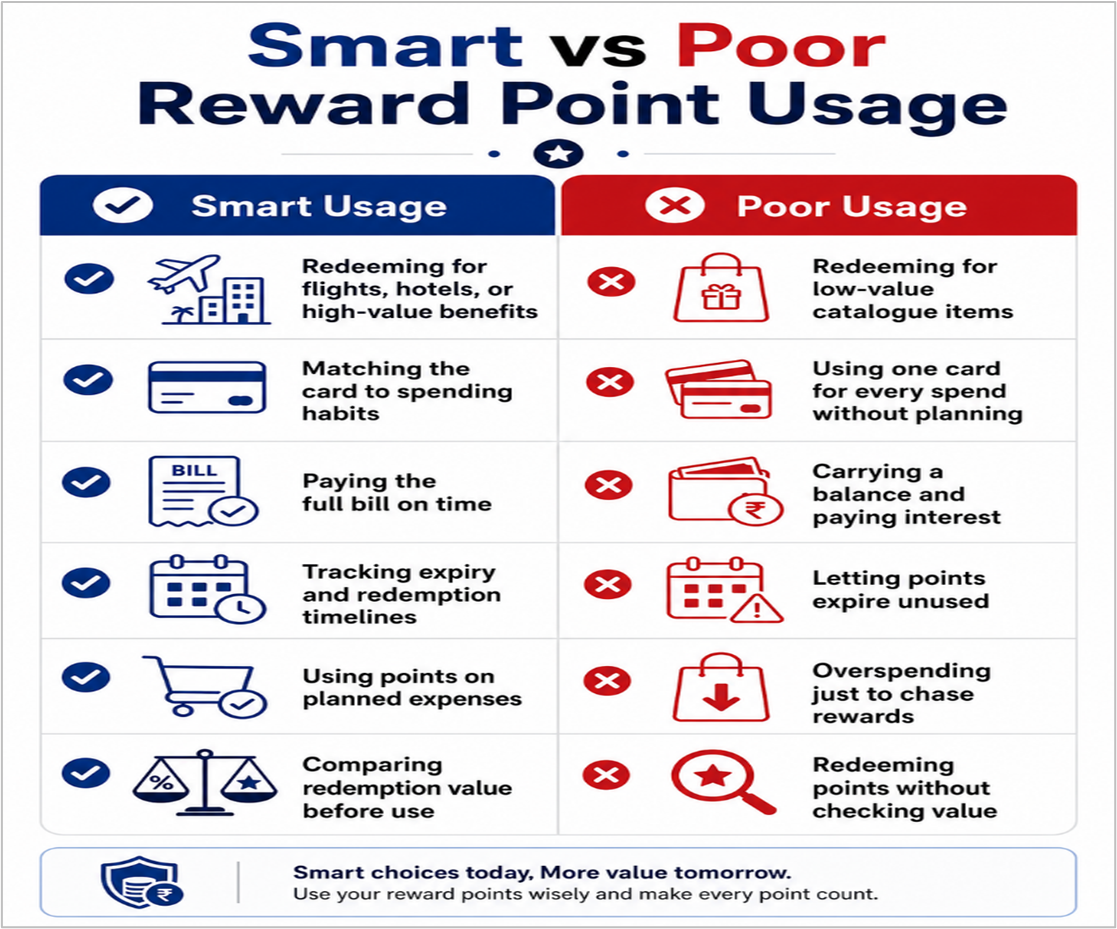

Common Mistakes People Make

The first mistake is not knowing the rupee value of points. Many users collect points for years without understanding whether they are getting ₹0.10, ₹0.25, ₹0.50 or more per point.

The second mistake is redeeming points only when they are about to expire. Last-minute redemption usually leads to poor choices.

The third mistake is ignoring annual fees, joining fees, redemption fees and convenience charges. A person may earn ₹5,000 worth of rewards but pay ₹4,000 in fees. The net benefit is only ₹1,000.

How To Make Reward Points Efficient

The efficient way is not to “hack” the system in a risky way. It is to use the rules better than the average user.

Start by necessary expenses on the card. Next, track points every month. Then calculate the value before redeeming. Avoid low-value redemptions unless convenience matters more than money. Use points for flights and hotels when cash prices are high. Book early because travel inventory can be limited. Compare points plus taxes with the full cash price. If the saving is meaningful, redeem. If not, pay cash and save points for a better opportunity.

For hotels, check whether points cover only the room or also taxes. For flights, check whether points cover the fare but not charges. For vouchers, check expiry dates. For cashback, check whether it is instant, statement-adjusted or delayed.

Credit Card Tiers Which Card Fits Which Spender?

Credit cards are not all designed for the same type of customer. Different card tiers offer different benefits, fees, reward rates and redemption options. A card that works well for a high spender may be unnecessary for a beginner. Similarly, a basic card may not give enough value to someone who spends heavily on travel, hotels or lifestyle categories.

A simple way to understand card tiers is by comparing them with monthly spending levels.

| Card Tier | Suitable Monthly Spend | Typical Features | Who It May Suit |

|---|---|---|---|

| Entry-level | Below ₹25,000 | Low or zero annual fee, basic reward points, simple cashback or vouchers | First-time card users, students, low spenders |

| Standard | ₹25,000–₹50,000 | Better everyday rewards, basic offers, possible annual fee waiver | Salaried users with regular monthly expenses |

| Premium | ₹50,000–₹1,00,000 | Better reward rates, travel benefits, lounge access, hotel/flight redemption options | Users with steady spends and occasional travel |

| Luxury | ₹1,00,000–₹2,00,000 | Higher reward potential, milestone benefits, stronger travel and lifestyle benefits | Frequent travellers and high monthly spenders |

| Ultra-luxury | ₹2,00,000+ | High annual fees, premium travel access, hotel privileges, concierge-style benefits, stronger partner redemptions | High spenders who can fully use premium benefits |

Source: pointsmax.in

The best card is not always the most premium card. The best card is the one where the user can naturally recover more value than the fees paid, without increasing unnecessary spending.

How to Choose the Right Card Tier

A cardholder should not choose a card only because it looks premium. The decision should be based on spending pattern, fee recovery and redemption behaviour.

| Monthly Spend Pattern | More Suitable Card Type | Reason |

|---|---|---|

| Low monthly spends and basic shopping | Entry-level | Low fees matter more than luxury benefits |

| Regular household spends, bills and shopping | Standard | Balanced rewards with manageable fees |

| Frequent online spends and some travel | Premium | Better reward structure and useful travel benefits |

| High travel, hotel and lifestyle spend | Luxury | Higher benefits may justify higher fees |

| Very high spends and frequent premium travel | Ultra-luxury | Premium perks may create meaningful value |

A practical rule is to compare the expected value of rewards with the annual fee. Estimate your likely spending, calculate the rewards you may earn in a year, convert them into a realistic cash value based on your redemption pattern, and compare that with the fee.

Source: community.finanjo.com

Conclusion

Credit card reward points are not free money; they have value only when redeemed well. They can expire, be devalued, or offer poor redemption options. The key is to earn rewards through your normal spending, not by spending more to chase points. For most users, a credit card should be a payment tool, not a source of credit. Pay your bill in full and on time, understand what your points are worth, and redeem them only when they deliver real savings. Reward programmes are carefully designed by banks, merchants, and payment networks. The benefit lies in understanding the rules better than the average user. The upside is turning everyday spending into meaningful savings; the downside is that fees, interest charges, poor redemptions, or overspending can easily erase those gains.

The real advantage is not finding the next deal; it is discipline. Spend as planned, pay on time, know your reward value, and redeem wisely. That's how rewards genuinely add value to your finances.

Anurag Patel, Associate Vice President - Customer Insight and Data Analytics, Kotak Mahindra AMC says:

“Credit Cards Rewards - Tool, not a Trap: Credit card reward points are neither a magic wealth-builder nor a hidden trap — they are simply a financial tool whose outcome depends entirely on the user. For disciplined spenders who pay bills in full and redeem points thoughtfully, rewards can quietly add meaningful value to everyday expenses. For those who overspend or carry balances, the same points can mask real costs and erode financial health. The card itself is neutral; the behaviour around it decides the outcome.”

Ronak Daga, Senior Manager - Equity Research, Kotak Mahindra AMC says: "Credit card reward points may appear to be a simple spending incentive, but they are part of a much larger economic ecosystem involving banks, merchants, payment networks, and loyalty partners. Their true value lies not in earning more points, but in using them strategically. When rewards are earned through planned spending, bills are paid in full, and points are redeemed efficiently, everyday expenses can translate into meaningful long-term savings.”

KMAMC is not guaranteeing/offering/communicating any indicative yield/returns on investments. The stocks/sectors mentioned do not constitute any kind of recommendation and are for information purpose only. Kotak Mahindra Mutual Fund may or may not hold position in the mentioned stock(s)/sector(s). Companies mentioned don’t constitute recommendation, brand name affiliation disclaimer & companies mentioned for illustrative purpose only. These materials are not intended for distribution to or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. The distribution of this document in certain jurisdictions may be restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

SEBI Registered Name - Kotak Mahindra Mutual Fund

SEBI Registered Number - MF/038/98/1