21 May 2026

Walk into any electronics store or scroll through an e-commerce app, and one offer almost always stands out “No Cost EMI.” A ₹30,000 smartphone, a ₹45,000 laptop, a ₹60,000 refrigerator, all available in easy monthly instalments, with no interest, or so it appears. The promise is simple and incredibly appealing: take home a product today, pay for it over time, and incur zero interest.

At first glance, it feels like a financial hack; almost like beating the system. But economics rarely allows a free lunch. If no interest is being charged, then who is paying for it?

The answer lies not in what is shown, but in what is subtly adjusted.

The Illusion of Zero

The idea of “No Cost EMI” is built on a clever reframing of cost rather than its elimination. The interest component hasn’t disappeared; it has simply been shifted or embedded elsewhere in the transaction. In many cases, the product you’re buying under a No Cost EMI scheme is priced slightly higher than its true market value. What appears as a discount is often equal to the interest that would have been charged. This “discount” is then passed on to the bank or financing partner as compensation for offering the EMI. So, while your invoice may say “0% interest,” the economic reality is different; you’ve already paid for that interest in the price itself.

Who Really Pays?

There are typically three players involved: the consumer, the merchant, and the bank. The cost is distributed among them in ways that are not always obvious. Sometimes, the merchant absorbs the interest cost. This might sound counterintuitive: why would a seller willingly reduce their margin? The answer lies in volume. Offering No Cost EMI significantly increases conversion rates. Customers who hesitate at a ₹30,000 purchase may feel comfortable paying ₹5,000 per month. For the seller, faster sales and higher volumes can outweigh the margin sacrificed. At other times, the bank earns through indirect means; processing fees, late payment penalties, or merchant commissions. Even when the interest appears to be zero, the financial ecosystem ensures profitability is maintained.

For Example: (For Illustration purpose only)

| Particulars | Upfront Payment | Standard EMI | No Cost EMI |

|---|---|---|---|

| MRP | ₹100,000 | ₹100,000 | ₹100,000 |

| Total Cost | ₹100,000 | ₹110,000 | ₹100,000–₹105,000 |

| Interest Charged? | No | Yes | Absorbed/restructured |

| Liquidity Impact | Full amount needed upfront | Spread over tenure | Spread over tenure |

| Cashback / Offers | Usually available | Usually available | Usually withheld |

| Credit Profile Impact | None | Yes — timely payment matters | Yes — timely payment matters |

| Processing Fee | None | None (interest is the cost) | Possible (₹3,000–₹5,000) |

| GST on Interest Amount | None | Charged | Charged |

| Foreclosure | Not Applicable | Lock-in for some time, post that can close | Penalty on closure |

| Option | Nature of Cost |

|---|---|

| Upfront Payment | Generally cheapest, no hidden cost |

| Standard EMI | Clear, visible interest |

| No Cost EMI | Looks free, may involve hidden cost (processing fees, GST on interest amount, foreclosure, etc.) |

When you opt for a “No Cost EMI,” the cost is not eliminated, it is simply shifted or hidden in different forms. First, you often lose the upfront discount. For example, the same product that costs ₹95,000 in a cash transaction is priced at ₹1,00,000 under EMI, effectively embedding ₹5,000 as hidden interest. Second, there are additional charges such as processing fees, typically around ₹3000–₹5000 including GST. While these may seem small individually, they increase the overall cost. Third, even though the scheme is marketed as “no interest,” banks internally calculate interest and levy GST on it, which adds roughly ₹5000 in this case. This cost is either included within the EMI structure or charged separately, making it less visible to the customer. Fourth, you also forgo other benefits such as credit card cashback or additional discounts that are usually available on single payments. This results in a further loss of about ₹1,500 in value. Fifth, and most importantly, there is an opportunity cost—perhaps the most overlooked factor. Lastly, there is a risk factor associated with delayed payments; even a single missed EMI can result in late payment charges and high penal interest, potentially costing an additional ₹500–₹2,000 or more.

The final understanding is simple: paying upfront is usually the cheapest and cleanest option with no future obligations; a normal EMI is transparent and clearly shows the cost of borrowing; while a No Cost EMI creates the perception of zero cost but actually recovers it through hidden adjustments, lost benefits, and foregone opportunities.

The Psychology Driving It

The real power of No Cost EMI isn’t just financial; it’s psychological.

Humans are wired to feel the “pain of paying.” A large, one-time payment feels like a loss, while smaller, spread-out payments feel manageable. By breaking a large expense into monthly installments, No Cost EMI reduces this psychological friction. There’s also the effect of anchoring. Instead of focusing on the total cost, your attention shifts to the monthly EMI. A ₹4,999 installment feels affordable, even if the total adds up to a significant amount. And perhaps most importantly, it taps into instant gratification. Instead of waiting months to save up, you can enjoy the product immediately. Future income is brought forward to fund present consumption. The below graphs tells you this story.

Source: https://razorpay.com/blog/indias-festive-fever-the-rise-of-emi/

https://www.techsciresearch.com/report/india-consumer-durable-finance-market/7478.html

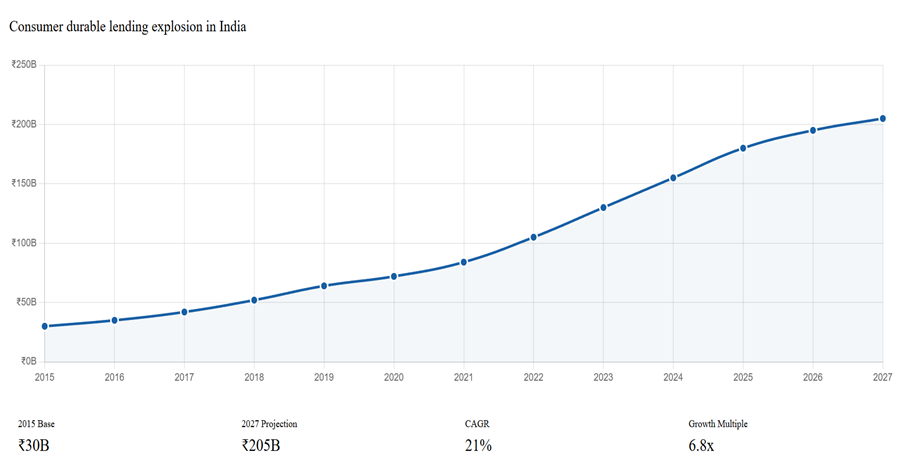

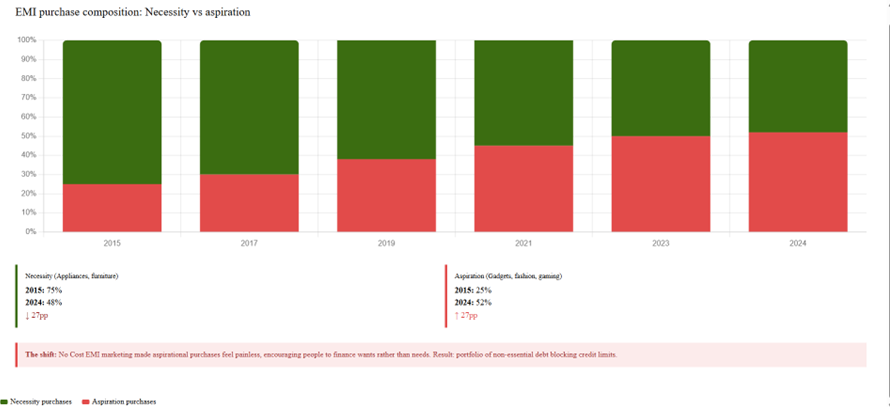

Over the past decade, consumer lending in India has seen strong and sustained growth, reflecting a sharp rise in credit-led consumption. The total size of consumer durable lending has increased from around ₹30 billion in 2015 to a projected ₹200+ billion by 2027, implying a nearly 6–7x expansion and a steady growth rate of about 20% annually. Initially, this growth was driven by financing for essential household items such as appliances and furniture. However, the nature of consumption has gradually shifted. In 2015, nearly 75% of EMI purchases were for necessities, while only 25% were for aspirational or discretionary items such as smartphones, gadgets, fashion, and lifestyle products.

Source:https://ibsintelligence.com/ibsi-news/how-india-borrows-2024-aspirational-loans-emi-cards-mobile-banking-soar/

Over time, this mix has reversed significantly. By 2024, the share of aspirational spending has risen to over 50%, overtaking necessity-driven purchases, which have declined to less than half of total EMI usage. This indicates a clear behavioural shift: consumers are no longer using credit just to meet essential needs but increasingly to upgrade lifestyles and fulfill wants. The rapid expansion in lending, therefore, is not just a story of penetration but also of evolving consumption patterns. A key driver behind this shift has been the rise of No Cost EMI offerings. These schemes have made high-value discretionary purchases appear more affordable by removing the psychological burden of interest costs, thereby encouraging consumers to spread payments over time without feeling the impact of borrowing. As a result, No Cost EMI has played a significant role in accelerating both the growth of consumer lending and the transition from need-based to aspiration-driven spending.

When It Makes Sense and When It Doesn’t

No Cost EMI isn’t inherently bad. In fact, it can be financially sensible under certain conditions. If the price of the product is genuinely the same as its upfront cost, and there are no hidden charges, spreading payments can help manage cash flow. It may even allow you to invest your savings elsewhere while paying in installments. However, the risks arise when the scheme influences your behaviour. If you’re buying something you wouldn’t have purchased otherwise, or if multiple EMIs start stacking up, the convenience can quickly turn into financial strain. Hidden costs such as processing fees or GST on interest components can also quietly erode the perceived benefit.

A Larger Economic Lens

On a broader level, No Cost EMI plays a significant role in modern consumption patterns. It fuels demand, especially in sectors like electronics, appliances, and lifestyle goods. By making products more “affordable” in the short term, it encourages spending and supports economic growth. At the same time, it subtly promotes a credit-driven culture, where consumption is increasingly decoupled from immediate income. While this boosts short-term demand, it can also lead to over-leverage and reduced savings discipline over time.

“No Cost EMI” doesn’t eliminate cost; it redistributes it. The interest hasn’t vanished; it has simply been hidden within pricing, absorbed by sellers, or compensated through other channels.

The next time you see a No Cost EMI offer, it’s worth pausing for a moment and asking a simple question: Would you still buy this if you had to pay the full amount today?

If the answer is yes, the EMI might just be a convenient payment option. But if the answer is no, then the offer isn’t saving you money; it’s influencing your decision.

Mrs Shibani Kurian, Senior Executive Vice President, Kotak Mahindra AMC adds : On one hand, our child’s education is a goal most of us have. On the other hand, Inflation in education is also reality. We have seen that education costs rise faster than average CPI inflation. The most effective tool to battle this is compounding. Early investing turns compounding into the most effective hedge against education cost inflation. Hence, investing early for your child’s education allows small, regular savings to grow steadily, reducing the pressure of large, last minute expenses when costs peak. The good news is— you don’t need big amounts if you start early and therefore starting a SIP is probably the smartest investment planning tool for all of us.

Disclaimers

KMAMC is not guaranteeing/offering/communicating any indicative yield/returns on investments. The stocks/sectors mentioned in this slide do not constitute any recommendation and Kotak Mahindra Mutual Fund may or may not have any future position in these sectors/stocks. These materials are not intended for distribution to or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. The distribution of this document in certain jurisdictions may be restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

SEBI Registered Name - Kotak Mahindra Mutual Fund

SEBI Registered Number - MF/038/98/1