6 May 2026

Packaging rarely makes headlines. Yet it quietly powers India’s consumption story, wrapping every biscuit, medicine strip, beverage bottle, e-commerce parcel, and export carton.

Traditionally, packaging was seen as a functional necessity, protecting products, enabling transport, and extending shelf life. Today, it has evolved into something far more strategic. Packaging now influences brand perception, consumer experience, sustainability outcomes, and supply chain efficiency.

In many ways, if India’s consumption story is a movie, packaging is the invisible scriptwriter, rarely seen, but shaping every scene.

The Under‑Penetration That Signals Opportunity

Despite strong growth, India remains materially under‑packaged relative to global peers.

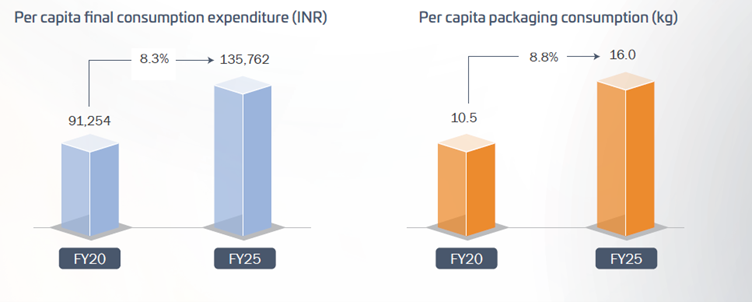

Packaging as a Mirror of India’s Growth

The relationship between consumption and packaging demand is almost mechanical: as India consumes more, it inevitably packages more.

Over the past five years:

- Per capita consumption grew at ~8.3% CAGR

- Per capita packaging consumption grew faster at ~8.8% CAGR

This led to:

- Packaging usage rising from 10.5 kg (FY20) to 16.0 kg (FY25) per capita

(Source: Avendus Capital, FY25–26)

Key Insight: Packaging doesn’t just follow consumption, it often leads it. Before products are sold, they must be packaged. This makes packaging a leading indicator of demand cycles, often moving ahead of headline GDP data.

Understanding the Packaging Industry

The packaging industry spans the design and production of materials used to protect, store, and transport products across sectors like food & beverages, pharmaceuticals, personal care, industrial goods, and e-commerce.

Types of Packaging

- Primary Packaging – Direct contact (e.g., shampoo bottle)

- Secondary Packaging – Groups products (e.g., cartons)

- Tertiary Packaging – Enables bulk transport (e.g., pallets, outer boxes)

Key Material Segments

- Plastic (rigid and flexible)

- Paper & paperboard

- Glass

- Metal

Each serves different functional and economic needs, balancing cost, durability, sustainability, and aesthetics.

Snapshot of The Global Packaging Industry

With rapid urbanisation, digitization, and environmental regulation reshaping consumer and industrial behaviour, packaging is undergoing a multi-dimensional transformation, from material innovation to supply chain reconfiguration.

(In USD Bn, Source: Avendus Capital, FY25–26)

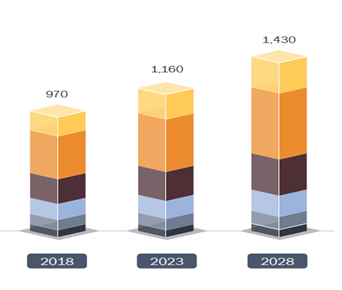

India’s Packaging Market: Scale and Opportunity

The Indian packaging industry is benefiting from strong demographic tailwinds, rising incomes, evolving consumer behaviour, and rapid formalisation of retail and supply chains. Closely linked to consumption volumes, it serves as a proxy for India’s long-term consumption growth. Its expansion is driven by every additional unit sold across FMCG, food, pharmaceuticals, durables, and e-commerce sectors.

- FY25 market size: ~₹5.4 trillion

- FY30E market size: ~₹8.3 trillion

- Growth: High single-digit CAGR, ~1.3x GDP growth

India’s Packaging Industry Size (INR Bn)

(Source: Avendus Capital, FY25–26)

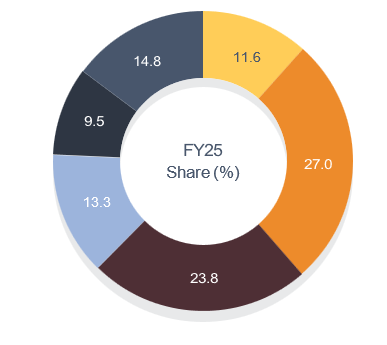

Substrate Mix (FY25)

(Source: Avendus Capital, FY25–26)

Despite its size, the industry remains highly fragmented, especially in flexible plastics and corrugated packaging—creating room for consolidation and scale-led efficiencies.

The Under-penetration Advantage

India’s packaging story is still in its early innings.

Per‑Capita Plastic Packaging Consumption

| Country / Region | kg per capita |

|---|---|

| United States | 110–115 |

| European Union | 65–70 |

| Germany | 40–45 |

| China | 45–50 |

| India | 14–16 |

Source: Avendus Capital, industry reports

This gap is structural, not cyclical.

As loose staples transition to branded products, as modern retail expands and as ecommerce penetration rises, even small increases in per‑capita packaging translate into massive incremental volume, especially when applied to a population of ~1.5 billion.

India doesn’t need to converge with developed markets to generate outsized growth. Even marginal progress offers a long runway.

Key Growth Drivers

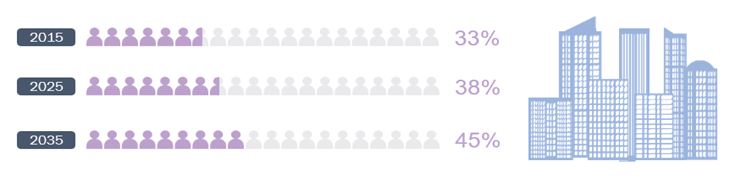

1. Rising Consumption and Urbanisation

Urban population is expected to rise from 33% (2015) to ~45% (2035E).

Urban consumers demand:

- Convenience

- Hygiene

- Shelf life

- Better presentation

All of which are packaging-intensive.

Urban population as a % of total population

Source: Avendus Capital, FY25–26)

2. Income Growth Inflection

India has crossed the USD 2,000 per capita income threshold—a point where consumption patterns structurally upgrade.

Globally, packaging demand grows 1.3–1.5x income growth beyond this level.

3. E-commerce and Quick Commerce

Packaging is now a logistics enabler, not just a container.

It must be:

- Durable

- Tamper-proof

- Optimized for returns

- Cost-efficient

This is driving strong demand for corrugated boxes, protective packaging, and mailers.

4. Food, Pharma, and Personal Care Expansion

- Packaged food demand is rising

- Healthcare requires sterile, tamper-proof packaging

- Personal care is driving premium formats

5. Branding and Premiumisation

Packaging is often the first consumer touchpoint. Better design, usability, and aesthetics directly influence purchase decisions.

Substrate Deep Dive: Where Growth Is Concentrated

Rigid Plastic Packaging (RPP): The Fastest Grower

- FY25 market size: ~₹625 bn

- FY25–30 CAGR: ~10.3%

- Key segments: bottles, preforms, caps, dispensers

India is now the fastest‑growing RPP market globally, driven by beverages, personal care and pharmaceuticals.

Source: Manjushree Technopack DRHP

Flexible Plastic Packaging (FPP): The Workhorse

- FY25 market size: ~₹1,458 bn

- FY25–30 CAGR: ~9.5%

- ~70% of India’s plastic packaging

Low cost and lightweight nature keep FPP dominant, though recycling rates remain below 10%, accelerating innovation toward recyclable mono‑material structures.

Paper & Corrugated: Sustainability‑Led Growth

- FY25 market size: ~₹1,286 bn

- FY25–30 CAGR: ~10%

Ecommerce, food service and plastic substitution are driving growth. Corrugated remains fragmented, while folding cartons are more organised.

(Source: Avendus Capital)

Glass and Metal: Premium and Resilient

Glass remains critical in pharmaceuticals and premium beverages; metal benefits from recyclability and industrial use cases. Growth is steady but capital‑intensive.

Sustainability: From Narrative to Economics

India’s Extended Producer Responsibility (EPR) framework is among the strictest globally.

Key mandates include:

- Mandatory collection and recycling targets

- Minimum recycled content (from FY26)

- Reuse norms for rigid plastics

Indicative Recycling Targets (FY30)

| Material | Target |

|---|---|

| Rigid plastics | ~75% |

| Flexible plastics | Sharp rise from <10% |

| Glass | ~50% |

| Metal | 40–45% |

| Paper | ~30% |

Source: Industry LCA studies, Avendus Capital

Carbon Footprint per Typical Pack

| Material | CO₂ emissions |

|---|---|

| Glass | ~750 g |

| Metal | ~450 g |

| Rigid plastic | ~150 g |

| Flexible plastic | ~45 g |

| Paper | ~45 g |

Source: Industry LCA studies, Avendus Capital

Contrary to popular perception, flexible plastics and paper have the lowest carbon footprints due to lightweighting—forcing a more nuanced sustainability debate.

Capital Flows and Consolidation

Packaging is emerging as a recession‑resilient investment theme:

- 86 transactions in the past decade

- 41 deals > USD 20 mn

- USD 5.6 bn total deal value

- Median EV/EBITDA: ~9x

Strategic buyers and private equity are targeting scale, export orientation and sustainability readiness.

Source: Avendus Capital

Risks That Cannot Be Ignored

Despite tailwinds, challenges persist:

- Fragmentation and pricing pressure

- High capex requirements

- Raw material volatility

- Execution risk on EPR compliance

The winners will be those who combine scale, innovation and regulatory discipline.

The Road Ahead: Three Defining Pillars

1. Sustainability

Designing for recyclability and minimal environmental impact will be non-negotiable.

2. Innovation

Material science, smart packaging, and design will drive differentiation.

3. Consumer-Centricity

Convenience, safety, and experience will shape packaging decisions.

India’s Invisible Growth Flywheel

Packaging may never be glamorous, but it is everywhere.

As India transitions:

- From loose to branded

- From basic to premium

- From limited choice to multiple SKUs (Stock Keeping Units)

Packaging intensity increases not gradually, but structurally. If you want to understand India’s consumption story, don’t just track what people buy.

Track how it is packaged.

Because packaging is no longer just about enclosing a product; it is about delivering value, enabling growth, and shaping the future of consumption.

Hrishikesh Bhagat, Vice President, Equity Research states that "In India’s evolving consumption landscape, packaging has shifted from serving a basic functional purpose to becoming an essential element of branding. This transformation presents a substantial and scalable opportunity to deliver greater value to consumers."

SEBI Registered Name - Kotak Mahindra Mutual Fund

SEBI Registered Number - MF/038/98/1

Disclaimers

The stocks/sectors mentioned do not constitute any kind of recommendation and are for information purpose only. Kotak Mahindra Mutual Fund may or may not hold position in the mentioned stock(s)/sector(s). These materials are not intended for distribution to or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. The distribution of this document in certain jurisdictions may be restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.