10 Apr 2026

India’s capital markets are steadily moving into a new phase of maturity. Rising household savings, a growing investor base, deeper equity markets and easier access to financial products are reshaping how Indians invest. At the centre of this transformation are asset management and wealth management companies, which are increasingly becoming the preferred channel for household savings.

The Foundation: A Strong and Stable Economy

India remains one of the fastest-growing large economies in the world. Compared to many global peers, India has shown consistent GDP growth and better economic stability. This matters because strong economic growth creates jobs, boosts incomes and increases savings.

As incomes rise, people naturally start thinking beyond daily needs. They look at long-term goals—education, buying a home, retirement and wealth creation. And that is where capital markets come into the picture.

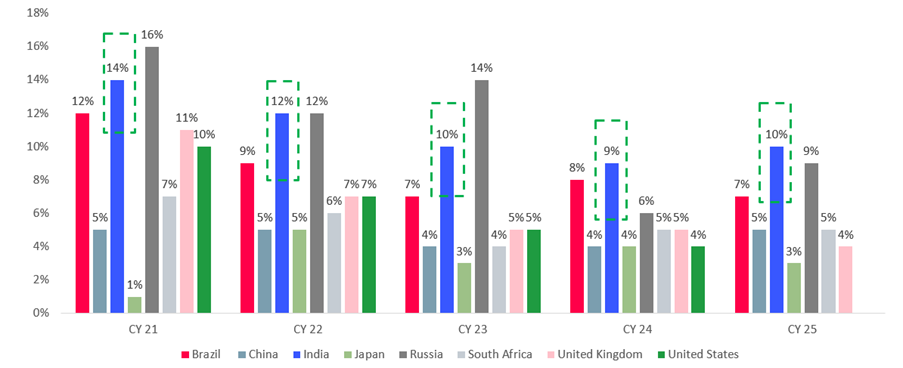

(GDP growth, % on year)

Note: All forecast are from IMF. GDP growth is based on current prices in national currency for each country. Estimated GDP growth for 2025.Source: IMF (World Economic Outlook – October 2025), As per latest data available

A supportive backdrop for financialisation

India’s economic fundamentals remain relatively strong compared with many global peers. Nominal GDP growth has stayed healthy, supporting income generation and the capacity to save. As economies grow and formalise, household savings tend to shift gradually from physical assets and low‑yield instruments towards capital market products.

India’s household savings have grown steadily over the years. In FY14, total household savings were around ₹23 trillion. By FY24, this number had more than doubled to over ₹54 trillion.

Source: Ministry of Statistics and Programme Implementation (MoSPI), As per latest data available

Household savings: Growing, but more importantly, changing

Household savings in India have grown at a steady pace over the last decade. More importantly, the composition of savings is evolving.

While bank deposits and insurance still account for a large share of financial assets, mutual funds are steadily gaining ground. Over recent years, the share of mutual funds in household financial savings has risen, while the share of deposits has moderated. This reflects increasing awareness of long‑term investing, improved access through digital platforms and a greater willingness to participate in market‑linked products.

This shift forms the foundation for long‑term growth in asset and wealth management.

Demographics provide long‑term visibility

India’s demographic profile continues to be a structural advantage. A large proportion of the population is in the working‑age bracket, with over two‑thirds below the age of 40. At the same time, mutual fund penetration remains low, indicating that a significant portion of the population is yet to enter formal market investing.

The combination of a young earning population and low penetration of financial products creates a long runway for growth over the coming decades.

Asset Management: Strong Growth, Low Penetration

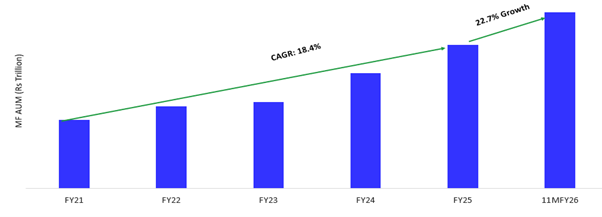

India’s mutual fund industry has reached a meaningful scale, with total assets under management (AUM) at approximately ₹82 trillion, of which equity AUM accounts for around ₹35 trillion, while monthly SIP inflows are ~₹299 billion.

The Indian mutual fund industry has expanded meaningfully over the past few years. Total industry AUM has grown at a strong pace, supported by a combination of rising inflows and market appreciation.

This growth is not confined to a single asset class. Equity, hybrid and passive strategies have all gained share, reflecting diversification in investor preferences. Importantly, mutual fund AUM as a proportion of bank deposits has also been rising, signalling deeper financialisation of household savings.

The industry has moved from being niche to mainstream, with scale that now allows sustained product innovation, distribution expansion and investor engagement.

Despite this strong growth, penetration remains low, as mutual fund AUM is only about 33% of bank deposits and just around 7% of Indian households invest in mutual funds. In contrast, globally, the gap is significant—particularly in the United States, where mutual fund AUM per capita rose from 16% of GDP in the late 1980s to about 70% by 2000, whereas India currently stands at around 20%, highlighting substantial headroom for future growth.

Source : NSE,BSE, SEBI, Data as of Feb’26, RBI, AMFI, I-Sec research report, ICI, Jefferies Research

Mutual Fund AUM growth highlights the scale of opportunity

Source: AMFI, Jefferies Research Report dated 5 Feb 2026. As per latest data available

Investor behaviour is becoming more disciplined

One of the most important changes in recent years has been the shift in how investors participate in markets. Rather than timing investments around market cycles, a growing number of investors are adopting disciplined, systematic approaches.

This behavioural change has played a key role in stabilising flows and supporting long‑term industry growth.

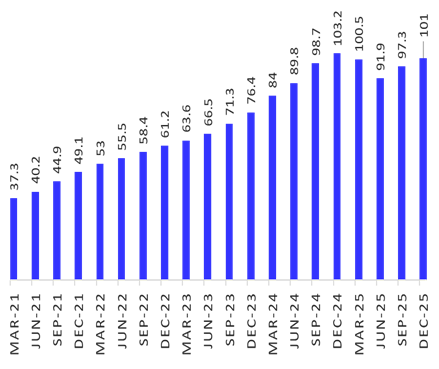

SIP growth reflects a structural behavioural shift

Source: SEBI, Equirus research report 10th Mar 2026

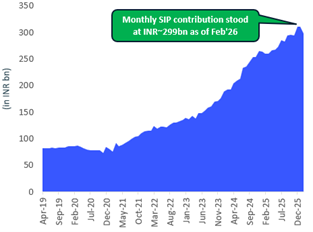

Systematic Investment Plans (SIPs) have emerged as a cornerstone of retail participation. The number of SIP accounts and monthly SIP contributions have risen steadily over time, even during periods of market volatility.

SIPs have helped investors smooth market cycles, reduce behavioural biases and remain invested through different phases of the market. For the industry, this has translated into more predictable and resilient flows.

Mutual fund investing in India is increasingly habit‑driven rather than event‑driven.

Participation is widening beyond large cities

Growth in the investor base is no longer limited to major metropolitan centres. While Tier I cities continue to account for a large share of industry assets, Tier II and Tier III cities are witnessing faster growth in unique investors.

Improved digital access, wider distributor networks and targeted investor education initiatives have helped broaden participation across geographies. This geographic diversification strengthens the sustainability of industry growth and reduces dependence on a few large markets.

Wealth management: Multiple models, broader reach

Alongside mutual funds, India’s wealth management industry is also evolving. Multiple business models coexist today, ranging from pure distribution and advisory‑led models to manufacturing‑plus‑distribution and transaction‑focused platforms.

These models cater to different investor segments, from mass affluent investors to ultra‑high‑net‑worth individuals. Over time, mass affluent and emerging affluent segments are expected to drive incremental growth, given their large numbers and rising incomes.

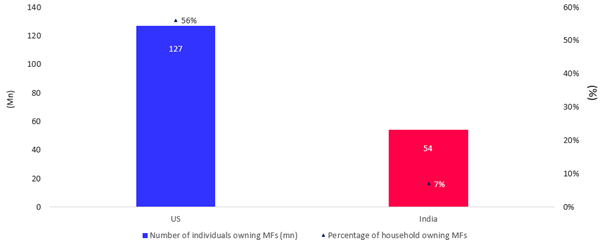

Low penetration underscores the long runway ahead

Source: Company reports, Kantar, Jefferies Research report 5th Feb 2026, as per latest data available

Despite strong growth, India remains at a relatively early stage of mutual fund penetration when compared with developed markets. The proportion of households owning mutual funds and mutual fund assets per capita remain significantly lower than in markets such as the US.

The opportunity ahead is structural. As incomes rise and financial awareness improves, participation is likely to deepen further over time.

Technology, alternates and the next phase of growth

Technology is playing an increasingly important role across asset and wealth management. Digital platforms have improved access and transparency, while automation and AI are enhancing productivity in areas such as research, reporting and compliance. Importantly, current AI adoption is productivity‑led rather than return‑led, with investment decisions remaining human‑driven.

At the same time, alternatives such as AIFs and PMS are emerging as important growth drivers, particularly among higher‑net‑worth investors seeking diversification beyond traditional equity and debt products.

The Long-Term Opportunity

When viewed together—strong economic growth, rising savings, increasing participation, low penetration, digital access, and regulatory strength—the direction is clear.

India’s capital markets, asset management, and wealth management industries are still in the early stages of a long growth journey.

This is not a story of quick gains. It is a story of:

- Consistent savings

- Disciplined investing

- Long-term compounding

The foundation is strong, participation is widening, and the runway remains long. For investors willing to stay invested, the most meaningful phase of growth may still lie ahead.

Umang Shah, Vice President, Equity Research at Kotak AMC adds: India is among the fastest growing economies in the world. India’s asset and wealth management industry is supported by strong macro fundamentals, rising wealth, greater financialization, technology adoption, and favourable demographics. Together, these factors create a compelling long-term opportunity for sustained growth.

Disclaimers

KMAMC is not guaranteeing/offering/communicating any indicative yield/returns on investments. These materials are not intended for distribution to or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. The distribution of this document in certain jurisdictions may be restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions. Kotak Mahindra Mutual Fund may or may not hold position in the mentioned stock(s)/sector(s).

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.