23 Apr 2026

Milk in India is more than a dietary staple; it is a cultural constant, a nutritional foundation, and a major economic pillar. From morning tea to curd set at home, dairy is present in our everyday life. Beneath this familiarity lies one of India’s most complex agrarian industries, supporting livelihoods at scale while navigating structural transformation.

India is the largest producer of milk globally, contributing around 24 percent of global milk production (Brickwork Ratings, April 2025; Basic Animal Husbandry Statistics 2024).

The Scale of India’s Dairy Economy

The Indian dairy market was valued at ₹18,975 billion in 2024 and is projected to grow at a compound annual growth rate of 12.35 percent, reaching ₹57,001.8 billion by 2033 (Brickwork Ratings, April 2025).

Milk production in India reached 239.3 million tonnes in FY2023–24, growing at a 5.62 percent CAGR between FY2014–15 and FY2023–24, driven almost entirely by domestic consumption (Brickwork Ratings 2025; BAHS 2024).

The dairy sector contributes around 5 percent to India’s national economy and directly supports over 80 million rural households, making it one of the country’s most employment‑intensive sectors (Brickwork Ratings, April 2025).

A Decentralised Producer Base

India’s dairy model is fundamentally decentralised. Milk production is dominated by small and marginal farmers, typically owning one or two animals. This structure gives dairy unmatched rural reach but also lowers per‑animal productivity and complicates standardisation.

Women play a central role within this system; their contribution is not incidental but structural.

Women Workforce: The Heart of India’s Dairy Economy

Women constitute nearly 70 percent of the workforce engaged in dairy farming activities in India, particularly in feeding animals, milking them, caring for them, and household‑level processing. Unlike many other agricultural activities, dairy provides women with regular, recurring participation in income generation, rather than seasonal engagement. (Sources: PIB, MOFPI(Ministry of Food Processing Industries of India); NDDB(National Dairy Development Board); Brickwork Ratings).

Institutionally, women’s participation has also increased. As of 2025, there are over 48,000 women‑led dairy cooperative societies operating at the village level, strengthening inclusion within the organised dairy network (PIB). NDDB has supported 23 Milk Producer Organisations, of which 16 are fully women‑run, covering approximately 1.2 million milk producers across 35,000 villages (NDDB via MOFPI).

Recognising this linkage, White Revolution 2.0 explicitly identifies women empowerment and employment generation as core objectives, integrating dairy expansion with rural livelihoods and cooperative participation (MOFPI; PIB releases 2024–25).

Roots of the White Revolution

India’s modern dairy transformation began with the establishment of the National Dairy Development Board in 1965, followed by Operation Flood in 1970, which replicated the Anand cooperative model nationwide (CARE Indian Dairy Industry Report). By 1988, India had overtaken the United States to become the world’s largest milk producer (NDDB).

NDDB’s designation as an Institution of National Importance in 1987 reinforced the cooperative backbone of Indian dairying (CARE Ratings).

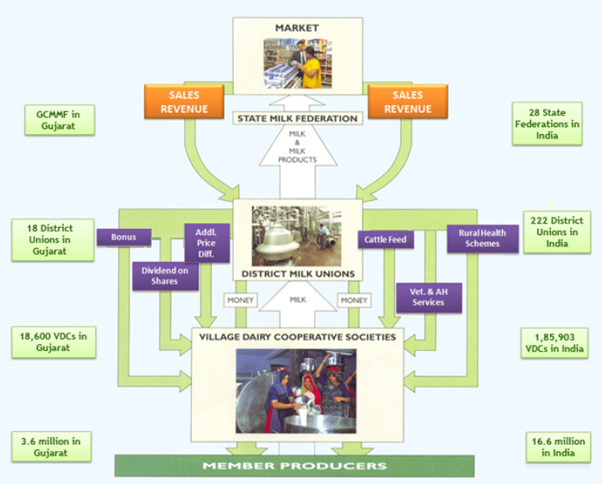

Amul: A Cooperative Success at Scale

Amul stands as one of India’s most enduring institutional successes, proving that cooperative ownership can scale without losing efficiency. Founded in 1946 in Anand, Gujarat, Amul began as a farmer response to high intermediary costs and evolved into the Gujarat Cooperative Milk Marketing Federation, built on a three‑tier structure of village societies, district unions, and a state federation (Source: Amul)

What started with two village societies and just 247 litres of milk now connects over 3.6 million milk producers across 18,000+ village cooperative societies, making it the world’s largest farmer‑owned dairy enterprise. Amul has scaled into a ₹1 lakh crore dairy and FMCG organisation, delivering assured procurement, transparent pricing, and daily income security to millions of small farmers, while competing successfully with private global consumer brands (Source: Fortune India, April 2026).

Source: Amul, the above process representation is for understanding and information purposes only.

Consumption Drives the System

India is both the world’s largest producer and consumer of milk. Almost all milk produced is absorbed domestically.

India’s fluid milk consumption is forecast at 221.37 million tonnes in calendar year 2026, broadly matching production levels (Source: USDA Dairy and Products Annual).

More than 45 percent of total milk production is consumed in liquid form, with the remainder processed into ghee, butter, curd, and milk powder. According to household survey data, Indian households spend close to 8 percent of total consumption expenditure on milk and milk products (Source: MOSPI Household Consumption Expenditure Survey 2023–24).

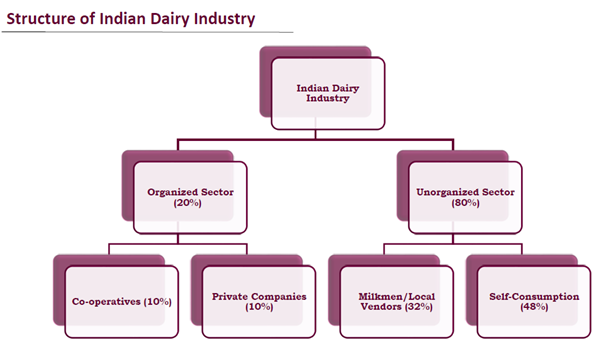

Organised Versus Unorganised

Despite its scale, India’s dairy sector remains largely informal.

The organised sector handles roughly 20 percent of milk, while around 80 percent flows through unorganised channels, including local vendors and self‑consumption (Source: CARE Indian Dairy Industry Report; Brickwork Ratings).

In comparison, over 90 percent of surplus milk in developed economies is processed through organised channels, highlighting the headroom for formalisation in India (Source: CARE Ratings).

Source: Brickwork report, April 2025.

Rise of Value‑Added Dairy Products

Growth momentum is increasingly shifting toward value‑added products such as ghee, paneer, cheese, yoghurt, flavoured milk, probiotic curds, and whey proteins.

These segments account for around 35–40 percent of the total dairy market value, despite relatively low penetration. Value‑added products offer substantially higher margins than liquid milk, often two to five times higher, making them central to future profitability (Source: CARE Indian Dairy Industry Report).

Exports Remain Limited

Despite being the largest producer, India contributes only around 0.25 percent of global dairy exports (Source: Brickwork Ratings).

This is explained by strong domestic demand, lower per‑animal yields, higher domestic price realisations, and quality compliance challenges in export markets (Source: USDA).

One exception is ghee exports. Indian ghee prices are 30–40 percent lower than European suppliers, offering competitiveness in markets such as Greece and Russia (Source: Crisil Dairy Monthly Dashboard, November 2025).

Policy Push: White Revolution 2.0

White Revolution 2.0, launched in 2024–25, aims to strengthen cooperatives and embed sustainability.

Key targets include:

- Formation of 75,000 new dairy cooperative societies

- Expansion of cooperative milk procurement to 1007 lakh kg per day by 2028–29

- Embedding circular practices such as biogas, organic manure, and cooperative feed supply

(Source: Ministry of Food Processing Industries; PIB releases 2024–25)

Digitising the Dairy Backbone

Digital systems are reshaping procurement and transparency.

- 35.68 crore livestock animals have been issued Pashu Aadhaar, enabling traceability and health monitoring (PIB Digitalising India’s Dairy Industry, Jan 2026)

- Over 26,000 dairy cooperative societies use Automatic Milk Collection Systems, enabling instant quality testing and payments (PIB; NDDB)

- 17.3 lakh milk producers benefit directly from digitised procurement systems (PIB)

GIS (Geographic Information System) based route optimisation initiatives have reduced transportation costs in multiple states (PIB).

Saumil Mehta, Senior Vice President, Equity Research – Equity Research, Kotak Mahindra AMC says, “Growing population, changing lifestyle patterns, increasing disposable incomes and increasing health consciousness makes dairy industry as one of the largest consumer discretionary plays and India’s dairy story is not just about milk — it’s about millions of livelihoods, the strength of cooperation and the power of nurturing a nation drop by drop”

Conclusion: The Next Phase

India’s dairy sector stands at a defining juncture. Its foundations are strong; deep farmer participation, rising domestic demand, and institutional strength. The next phase of growth will depend on value addition, formalisation, technology adoption, and sustained inclusion, particularly of women who form the backbone of daily dairy operations.

If India succeeds in aligning productivity with inclusivity and scale with sustainability, dairy will remain one of the country’s most resilient and equitable growth engines.

Disclaimers:

The stocks/sectors mentioned do not constitute any kind of recommendation and are for information purpose only. Kotak Mahindra Mutual Fund may or may not hold position in the mentioned stock(s)/sector(s). These materials are not intended for distribution to or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. The distribution of this document in certain jurisdictions may be restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions. Use of the company/ brand names does not imply any affiliation with or endorsement by them or any of its holding companies, subsidiaries or affiliates and are used for illustrative purpose only.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.