12 Mar 2026

In an increasingly uncertain world, defence spending is no longer discretionary—it is structural.

As global conflicts reshape military doctrines and technology priorities, India’s defence sector is undergoing a transformation that goes well beyond incremental budget increases. From indigenisation and electronics‑led warfare to exports and private‑sector scale‑up, the sector is being re‑engineered for sustained growth.

The result is a defence ecosystem that is strategic by necessity and industrial by design—with implications that extend far beyond national security.

Capital Allocation Signals a Structural Upcycle

The FY26–27 defence budget is pegged at ₹7.84 trillion, which is about 15% of the Union Budget and reflects a ~15% YoY increase over FY26 BE; it is also stated to be around 2% of estimated FY27 GDP. The most important quality shift is in capital expenditure: capital spending/capital outlay is ~₹2.19 trillion, representing a ~21.8% increase over FY26 BE, and lifting capital spending to about 28% of overall defence expenditure—a clear signal of higher modernisation intensity. The report further highlights that the Ministry of Defence has earmarked 75% of the capital acquisition budget for procurement from domestic industry, implying a structurally supportive environment for Indian defence manufacturers and indicating that budget availability is unlikely to be a constraint if execution and ordering timelines improve.

Crucially, the Ministry of Defence has earmarked ~75% of capital procurement for domestic sourcing, ensuring that higher allocations directly benefit Indian manufacturers rather than imports.

Source: Antique Stock Broking

From Budget Intent to Order Visibility

Budget intent translates into execution visibility via Defence Acquisition Council (DAC) approvals. During FY26, DAC accorded Acceptance of Necessity (AoN) worth ₹3.3–3.6 trillion, covering aircraft, missiles, naval platforms, drones, electronic warfare systems and sustainment programmes. This approval value is nearly 2× annual defence capital outlay, creating a deep, multi‑year pipeline.

Source: Defence & Aerospace – Sector Update, B&K Securities, 16 Feb 2026; ICICI Securities Defence Digest, Jan 2026

Major DAC AoN Approvals (FY26)

| Period | AoN Value (₹ bn) | Key Categories |

|---|---|---|

| Jul–Aug 2025 | ~1,700 | Missiles, EW, naval systems |

| Oct–Dec 2025 | ~1,600 | Pinaka, Astra Mk II, drones |

| Feb 2026 | ~3,600 | MRFA (Rafale), P8I, combat missiles |

Source: B&K Securities; ICICI Securities

Historically, AoNs convert into executable orders over 2–4 years, smoothing revenue visibility and reducing cyclicality across defence PSUs and private players.

Source: Motilal Oswal Defence Report, Dec 2025

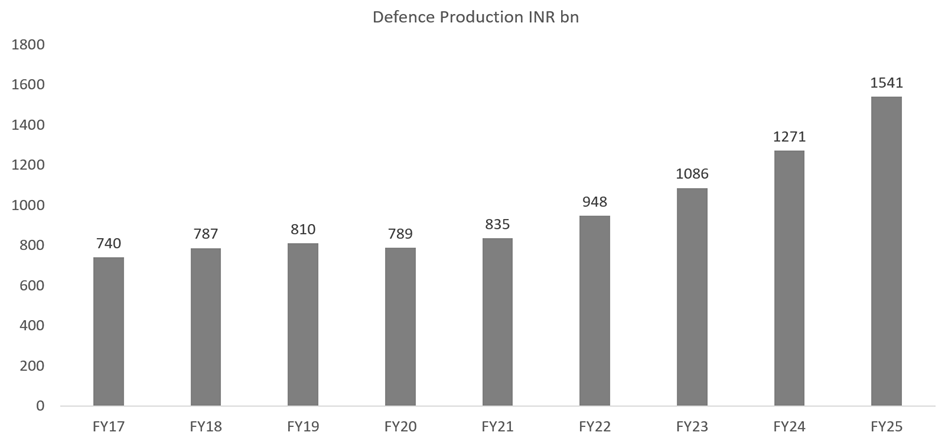

Indigenisation Moves From Policy to Production

Aatmanirbhar Bharat is not just a slogan, but a war cry. India’s indigenisation drive has moved decisively from policy articulation to on‑ground execution. Reforms under the Defence Acquisition Procedure (DAP), positive indigenisation lists, and Make‑I/II categories have reshaped procurement, favouring domestic design, development and manufacturing.

Source: Defence & Aerospace – Thematic Report, B&K Securities, 08 Dec 2025

Growth in Domestic Defence Production

Source: Antique Stock Broking

Importantly, indigenisation is no longer PSU‑only. Private players and MSMEs now contribute meaningfully across electronics, propulsion, structures and energetics, improving cost competitiveness and shortening delivery cycles.

Source: Defence & Aerospace – Sector Update, B&K Securities, Feb 2026

The transition is also clearly visible at the company level. Hindustan Aeronautics Limited is scaling up execution across fighter aircraft and helicopters while building capability for next‑generation platforms, anchoring India’s aerospace ambitions. Bharat Electronics Ltd is deepening its role in defence electronics—spanning radars, electronic warfare, communications and counter‑drone systems, reflecting the shift towards network‑centric warfare. Bharat Dynamics Ltd continues to expand missile and ammunition manufacturing aligned with rising domestic orders. In the naval segment, Mazagon Dock Shipbuilders Ltd and Garden Reach Shipbuilders & Engineers Limited are executing large warship and submarine programmes while adding capacity for future orders. At the same time, private players such as Solar Industries India Ltd and Bharat Forge Limited are moving up the value chain—from ammunition and energetics to artillery systems, drones and defence subsystems—signalling a broader and more diversified defence manufacturing ecosystem.

Source: Company data

Technology and Innovation Redefine Defence Growth

A defining feature of the current cycle is the institutionalisation of defence innovation.

AI is increasingly being integrated into unmanned systems and drones for autonomous navigation, target recognition and real‑time data processing; electronic warfare, radars and sensors for automated threat detection, signal classification and situational awareness; and C4ISR architectures to enable faster data fusion and decision support across joint operations.

Platforms such as iDEX (Innovations for Defence Excellence) and the Make‑I/II framework enable start‑ups and private firms to participate in defence R&D, particularly in drones, loitering munitions, AI‑enabled surveillance, cyber security, space‑based ISR and counter‑UAS systems.

Source: Defence & Aerospace – Thematic Report, B&K Securities; India’s Defence Industrial Sector Vision 2047, KPMG–CII

India’s defence corridors in Uttar Pradesh and Tamil Nadu further anchor this ecosystem by integrating testing facilities, manufacturing units and R&D infrastructure. Emphasis on dual‑use technologies enhances commercial viability and accelerates scale‑up.

Source: India’s Defence Industrial Sector Vision 2047, KPMG–CII, May 2025

Technology Shift Is Redefining Defence Demand

Modern warfare is increasingly electronics‑ and data‑centric. Recent conflicts have highlighted the importance of drones, electronic warfare, AI‑driven intelligence, precision munitions and C4ISR networks, shifting demand away from standalone platforms to integrated systems.

Source: Defence & Aerospace – Thematic Report, B&K Securities, 08 Dec 2025

Key Technology‑Led Demand Areas

| Segment | Demand Driver |

|---|---|

| Defence electronics | EW Suites, radars, communication systems, C4I systems |

| Drones & UAVs | ISR, loitering munitions |

| Missiles & ammo | Ammunition intensive warfare |

| Software & AI | Network centric operations |

Source: B&K Securities

EW stands for Electromagnetic Warfare, C4I: Command, Control, Communication, Computer and Intelligence, ISR stands for Intelligence, Surveillance, and Reconnaissance

This shift structurally favours India, where electronics and systems integration offer higher localisation potential than traditional heavy platforms.

Source: Defence & Aerospace – Sector Update, B&K Securities, Feb 2026

Global Factors That Are Favourable

Rising global geopolitical tensions have triggered a sustained increase in defence spending across developed economies, particularly among NATO members, many of whom are accelerating re‑armament and replenishing depleted inventories of ammunition, missiles and electronic systems. NATO’s renewed focus on higher defence allocations and supply‑chain diversification is expanding demand for reliable, cost‑competitive suppliers beyond traditional Western OEMs. This global re‑stocking cycle is creating a meaningful export opportunity for India, especially in areas such as missiles, ammunition, radars, electronic warfare and subsystems, where domestic capabilities have matured and delivery timelines are increasingly competitive. As global defence spending remains structurally elevated, external demand is emerging as a durable second engine of growth for India’s defence manufacturing ecosystem.

Source: Defence & Aerospace – Thematic Report, B&K Securities, 08 Dec 2025; Defence & Aerospace – Sector Update, B&K Securities, 16 Feb 2026; ICICI Securities Defence Digest, Jan 2026

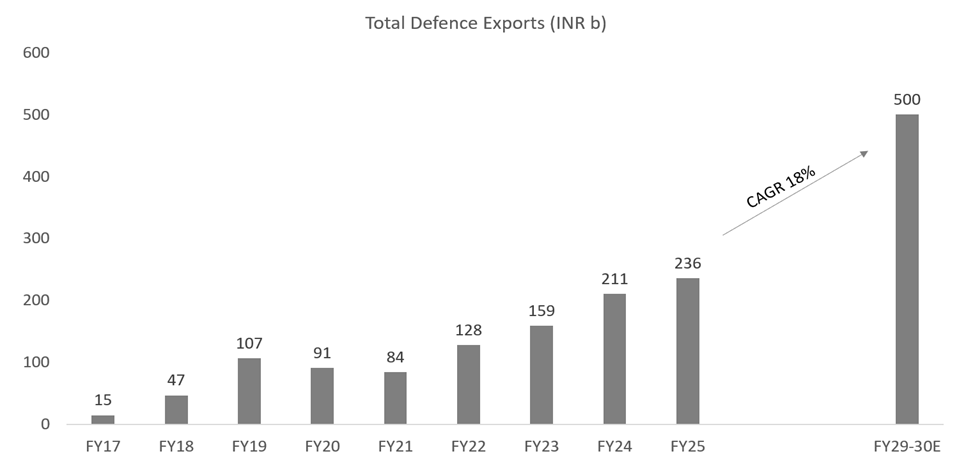

Exports: The Next Structural Growth Lever

The LCA Tejas Mk‑1A has become central to the Indian Air Force’s fighter modernisation, with over 180 aircraft on order, anchoring a domestic aerospace ecosystem with rising indigenous content and production depth. On the missile side, the BrahMos supersonic cruise missile has emerged as India’s most prominent defence export, with deliveries to the Philippines under a $375 million contract and growing interest from other Indo‑Pacific partners validating India’s export credibility. In parallel, systems such as the Akash air‑defence missile and Pinaka multi‑barrel rocket launchers have found overseas buyers, notably in Armenia, underscoring how India’s defence push is translating from policy and procurement into globally deployable, export‑ready platforms.

India’s defence exports have expanded over ten‑fold in the past decade, reaching ₹23,000–30,000 crore in FY25. The government targets ₹50,000 crore by FY29, supported by export facilitation, G2G (Government to Government) agreements and improving credibility of Indian platforms.

Source: ICICI Securities Defence Digest, Jan 2026; KPMG–CII Defence Vision 2047

India Defence Exports Trend

Source: DDP, MOFSL

Top Buyers from India

| Country | Nature of imports from India |

|---|---|

| Armenia | Akash missiles, artillery systems, electronics, software |

| France | Electronics, software components |

| USA | Materials, alloys, components, subsystems |

| UAE | Artillery ammunition, potential BrahMos interest |

| Philippines | BrahMos missiles, Akash missiles |

| Saudi Arabia | 155mm artillery shells |

| Vietnam, Brazil, etc. | Interested in BrahMos missiles and other Indian systems |

Source: B&K Research

As the US–Iran conflict intensifies, global geopolitical tensions have increased markedly. Historically, periods of heightened geopolitical risk prompt nations to raise military preparedness and fast‑track defence procurement.

Execution Risks: The Fine Print

Despite strong tailwinds, defence execution remains complex. Long gestation cycles, testing and certification delays, and working‑capital intensity, especially for private players, can impact near‑term cash flows.

Partial dependence on imported subsystems such as aero‑engines also poses supply‑chain risks, though localisation efforts are steadily mitigating these constraints.

Source: Defence & Aerospace – Thematic Report, B&K Securities, Dec 2025

Why This Cycle Is Fundamentally Different

Unlike earlier defence upcycles, the current phase is driven by domestic sourcing mandates, diversified AoN pipelines, technology‑led warfare demand, private sector participation and export validation. Defence spending is now embedded within India’s long‑term strategic and industrial policy framework, improving durability and visibility.

Conclusion: A Sector With Strategic and Economic Gravity

India’s defence sector has crossed a decisive inflection point. Backed by sustained capital allocation, multi‑year order visibility, accelerating indigenisation, innovation‑led demand and growing exports, it is evolving into a structurally resilient industrial ecosystem. While execution challenges persist, the foundations for multi‑decade growth are firmly in place, making defence not just a strategic necessity, but a core engine of India’s manufacturing and technology ambitions.

Mr. Dhananjay Tikariha, Sr. Vice President, Kotak Mahindra Asset Management Company Ltd and Equity Fund Manager adds “A robust domestic defence industry is essential for strategic autonomy and national security. India’s push for strategic autonomy has transformed defense from a traditional cost centre into a high-. Beyond near‑term order visibility, the sector offers a compelling medium‑to‑long‑term opportunity driven by indigenisation, exports and technology depth. Importantly, defence manufacturing delivers multiplier benefits across MSMEs, skilled employment, R&D and advanced manufacturing.”

Disclaimers:

KMAMC is not guaranteeing/offering/communicating any indicative yield/returns on investments. The stocks/sectors mentioned in this slide do not constitute any recommendation and Kotak Mahindra Mutual Fund may or may not have any future position in these sectors/stocks. Companies mentioned don’t constitute recommendation, brand name affiliation disclaimer & companies mentioned for illustrative purpose only. Use of the company brand names does not imply any affiliation with or endorsement by them or any of its holding companies, subsidiaries or affiliates and are used for illustrative purpose only.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.