14 May 2026

India’s southwest monsoon is more than just a weather change. It is a key driver of the country’s economy. The monsoon delivers nearly 70% of India's rainfall and supports the farming sector, which contributes about ~18% to the ~$4 trillion economy and provides livelihoods to nearly half the population. When the rains are weak, crops like rice, cotton, and soybeans can be affected. Lower rainfall also reduces soil moisture, which can impact winter crops such as wheat and rapeseed.

Its impact goes beyond agriculture. The monsoon influences rural incomes, food prices, and overall economic activity. Even though irrigation, supply chains, and policy support have improved over time, the June to September rains still play a major role in shaping outcomes across the country.

After two consecutive La Niña years (CY24–CY25) that delivered above-normal rains, the ENSO cycle is turning. Leading meteorological agencies now indicate a high probability of El Niño conditions in CY26, raising the risk of a below-normal monsoon.

Why the forecast is drawing attention

The biggest reason for concern is the possible return of El Niño conditions during the monsoon season. The official agency’s forecast adds credibility. It does not guarantee the outcome, but it does suggest the climate setup is not especially favorable for a strong monsoon.

The IMD may revise its view later in May, and monsoon predictions often change as the season approaches. So, the April forecast should be read as a warning, not as a final verdict. The real picture will become clearer once the monsoon sets.

IMD and Skymet: Comparative monsoon forecast outlook

| Parameter | IMD Forecast | Skymet Forecast |

|---|---|---|

| Overall Seasonal Forecast | Below Normal | Below Normal |

| Quantitative Estimate | 92% of LPA | 94% of LPA |

| Model Error Margin | ±5% of LPA | ±5% of LPA |

| Deficient Probability (<90% LPA) | 35% | 30% |

| Below-Normal Probability (90–95% LPA) | 31% | 40% |

| Above Normal + Excess | 7% | 10% |

| ENSO Assessment | El Niño very likely JAS | El Niño early in season |

| IOD Assessment | Positive IOD likely towards end of season | Neutral or delicately positive IOD; limited offset |

Source: IMD, Skymet, telegraphindia.com, IIFL Research

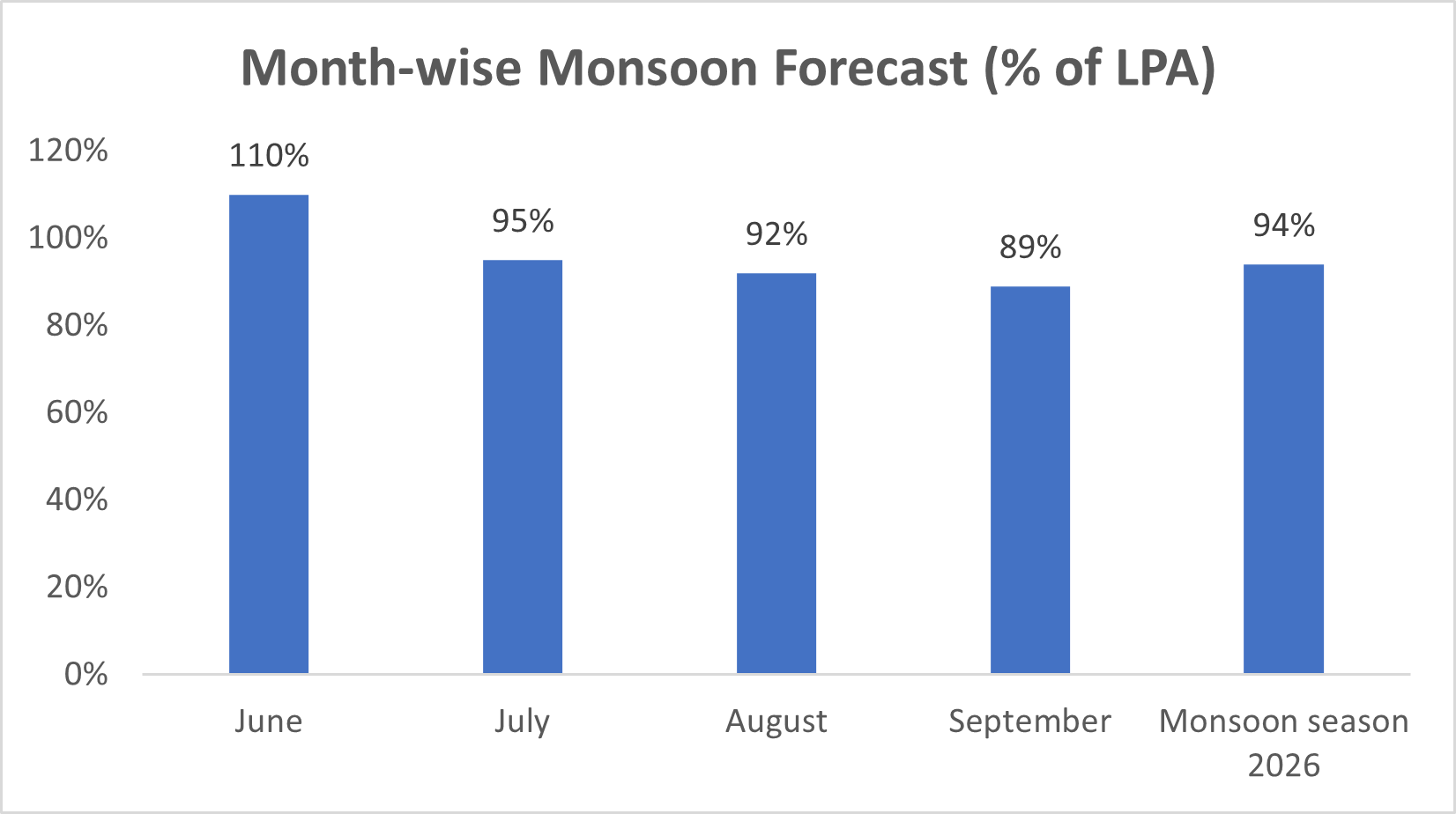

More important than the aggregate number is the intra-seasonal pattern. June is expected to be broadly normal, suggesting a reasonable onset. In contrast, rainfall risks rise meaningfully in the second half, with July and August projected below LPA, and September carrying the highest likelihood of deficiency. The IMD’s long-range forecast, placing rainfall closer to ~92% of LPA, broadly aligns with this assessment.

Source: Skymet, 360 ONE Asset Research, Business Standard

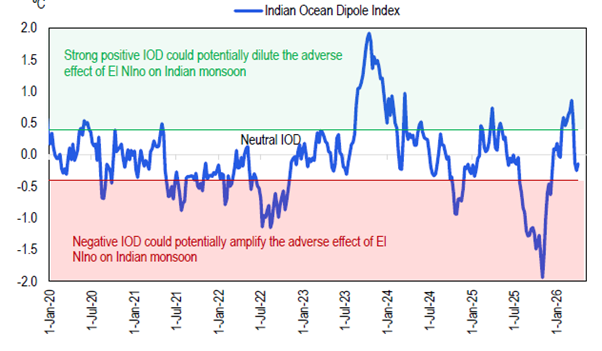

El Niño Returns: The Main Risk Factor

The primary climatic risk shaping the 2026 monsoon outlook is the anticipated return of El Niño conditions. El Niño—characterised by warmer-than-normal sea surface temperatures in the central and eastern Pacific—has historically weakened monsoon circulation over the Indian subcontinent.

Climate agencies and private forecasters expect El Niño to develop early in the season and strengthen during July–September, increasing the likelihood of rainfall shortfalls during the most critical phase of the monsoon. However, meteorologists consistently warn against simplistic conclusions. El Niño does not automatically imply drought—its eventual impact depends on timing, intensity and interaction with other climate drivers, especially the Indian Ocean Dipole (IOD). For 2026, the IOD is expected to remain neutral to mildly positive, offering only limited mitigation.

Source: Citi Research, Australian Bureau of Meteorology. This is as per the latest data available.

Why Averages Can Be Misleading

Historical experience shows that a weak monsoon does not mechanically translate into higher inflation or weaker growth. What matters far more than the seasonal average is the timing and regional distribution of rainfall.

There have been episodes when excess rainfall coincided with elevated food inflation, and others where deficient rainfall had limited economic impact. Outcomes depend largely on:

- Rainfall during crop-critical sowing and growth phases

- Concentration of rainfall deficits across key agricultural regions

- Size of foodgrain buffers and procurement effectiveness

- Efficiency of supply chains and timely trade interventions

In short, where and when it rains often matters more than how much it rains.

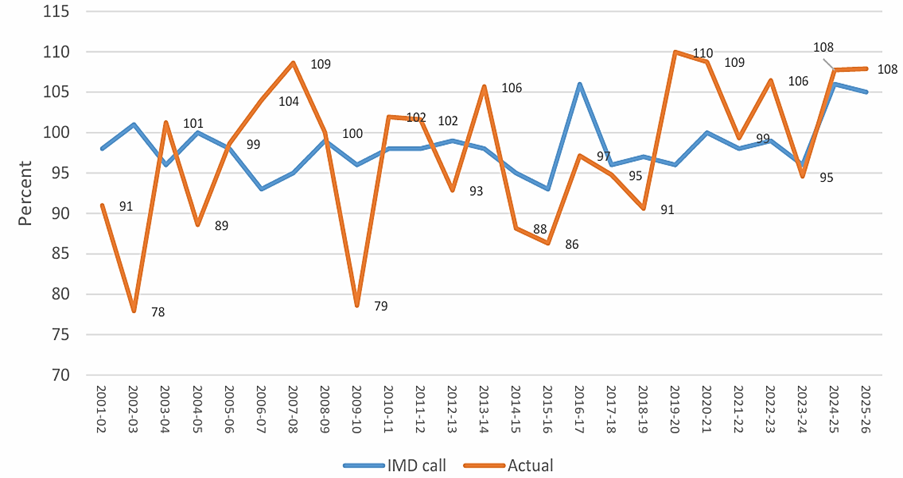

IMD's first call and Actual as % LPA

Source: IMD, Bob Research

Spatial distribution: Critical to monsoon impact assessment

The 2026 monsoon is forecast to be slightly weak at 92–94% of LPA, with a clear north–south divergence. Northern and central states—including Punjab, Haryana, Rajasthan, UP and MP—face higher rainfall risk, especially later in the season, which could affect Kharif sowing. In contrast, southern states such as Telangana, Andhra Pradesh, Karnataka and Kerala are expected to receive near‑normal rains, helping offset the overall agricultural impact.

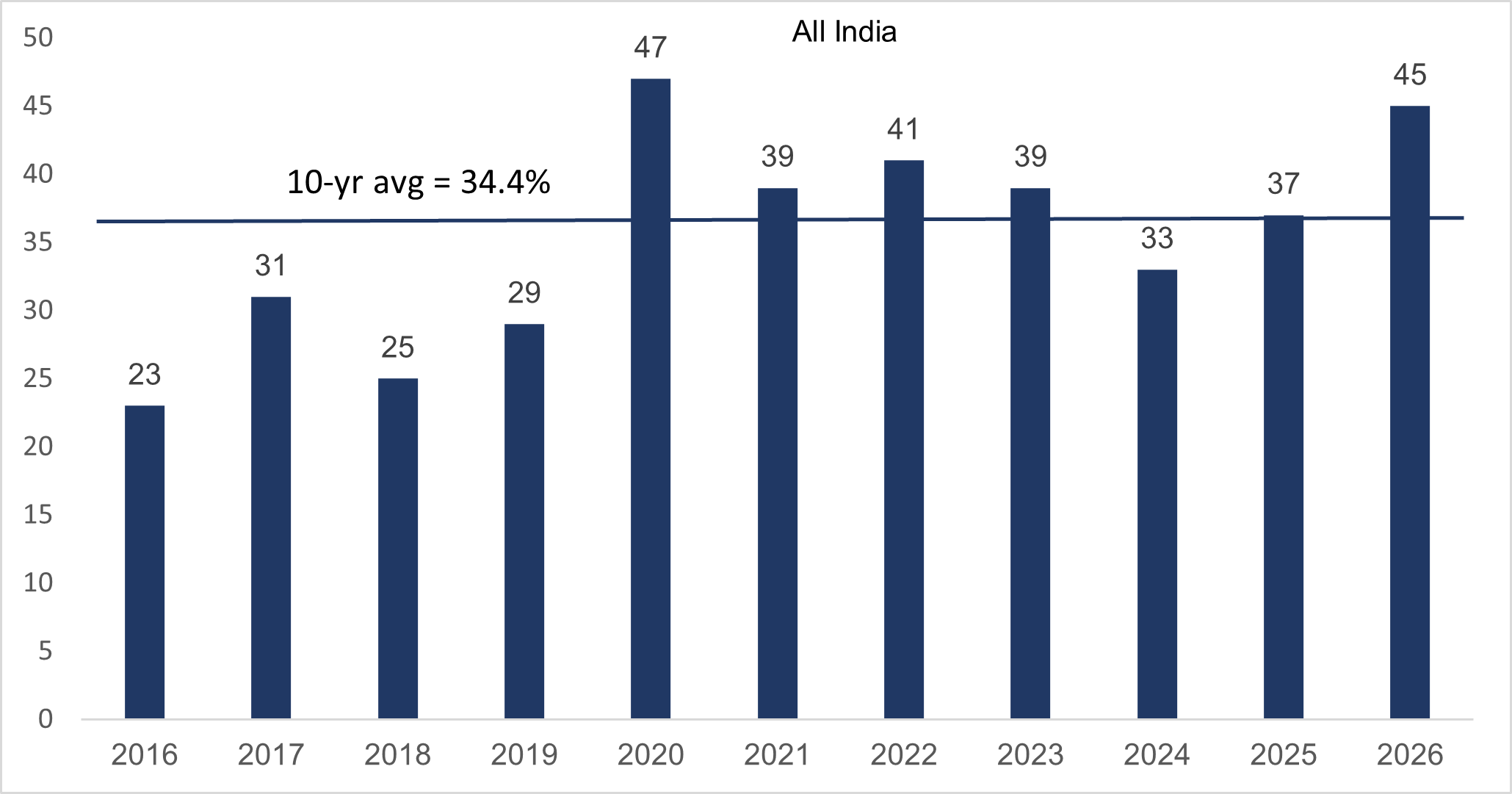

Above-average water reservoir levels provide cushion

As of early April 2026, reservoir levels stood at 44.6% of live capacity, well above the 10-year average. Historically, agricultural outcomes correlate more with storage levels than rainfall alone, implying that monsoon stress—if any—may show up with a lag.

Reservoir level as a percentage of live capacity- All – India

Source: CWC, CEIC, CLSA.

Inflation Impact: Food Is the Key Channel

Food accounts for ~37% of CPI, making it the most direct transmission channel. Currently:

- Edible oils show upward pressure

- Cereals and pulses remain stable

- Vegetable prices moderated in March–April

However, past El Niño years show sharper seasonal spikes in vegetable inflation, and a similar pattern in 2026 could add ~20–25 bps to headline CPI, even if other food categories remain contained.

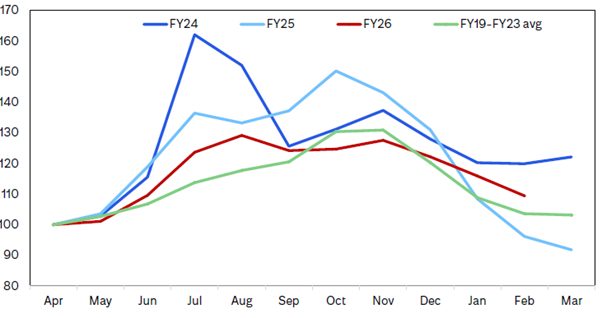

Vegetable CPI

Source: Citi Research, MoSPI

Summer-monsoon period seasonal increase in vegetable CPI during El Niño year FY24 was around twice the usual increase

Growth and Rural Demand: Pressure, not a Collapse

While agriculture’s direct share in GDP has declined structurally, its influence on rural demand remains significant. A weak monsoon can soften farm incomes, rural wage growth and discretionary spending on FMCG products, two-wheelers, tractors and entry-level housing.

That said, evidence from recent decades suggests that El Niño on its own has had a limited impact on aggregate GDP growth, unless accompanied by severe drought conditions. Studies indicate that a combined El Niño plus drought scenario may shave 20–65 basis points off growth, while moderate rainfall deficits typically result in temporary and uneven effects, rather than a broad-based slowdown.

Policy Buffers Remain Strong

India enters Monsoon 2026 with stronger shock absorbers:

- Higher irrigation coverage

- Elevated fertiliser subsidy outlays

- Comfortable foodgrain stocks

- Healthy reservoir levels

- Ongoing rural support schemes (PM-KISAN, MGNREGA, e-NAM)

These factors meaningfully reduce the inflation and growth sensitivity to rainfall shocks.

Historical Context: Weak Monsoons Are Not Unusual

Since the early 2000s, India has experienced below-normal monsoons every 3–4 years. Episodes such as 2015–16 saw limited macro damage due to buffers, while 2023 saw elevated food inflation largely due to uneven rainfall distribution—reinforcing that headline rainfall alone is a poor predictor of stress.

All‑India Southwest Monsoon Performance: Selected Years

| Year | Rainfall (% of LPA) | Classification | Key Outcome |

|---|---|---|---|

| 2002 | ~81% | Deficient | Severe drought; sharp agricultural stress |

| 2008 | ~98% | Normal | Good overall season despite intra seasonal volatility |

| 2009 | ~78% | Deficient | Major crop losses; rural demand slowdown |

| 2014 | ~88% | Below normal | Uneven rainfall; inflationary pressure |

| 2015 | ~86% | Below normal | Strong El Niño; limited GDP impact due to buffers |

| 2018 | ~91% | Below normal | Mild impact; agriculture GVA positive |

| 2023 | ~94% | Below normal | Food inflation spike due to uneven distribution |

| 2026E | ~92–94% | Below normal | Risk tilted to July–September weakness |

Source: India Meteorological Department (IMD), End‑of‑Season Monsoon Reports; Skymet Weather; RBI Bulletin, Yes securities

The Reserve Bank of India (RBI), in its research on weather and macro outcomes, highlights that the relationship between rainfall shortfalls and economic variables has weakened over time, reflecting better irrigation, diversification of rural incomes, and policy interventions. [rbi.org.in]

In other words, a below‑normal monsoon in 2026 would not be unusual in historical terms, but its eventual impact will depend far more on distribution and persistence rather than the headline seasonal average.

Why India Is Better Positioned Today

Compared with earlier decades, India enters the 2026 monsoon season with stronger shock absorbers:

- Higher irrigation coverage and more diversified cropping patterns

- Large foodgrain buffers and assured MSP mechanisms

- A rising share of non-farm income in rural areas

- Improved logistics, imports flexibility and supply-chain management

- Stronger overall macro-policy credibility

These factors have steadily weakened the traditional link between rainfall shortfalls and economic outcomes.

What Matters Going Forward:

Rather than focusing solely on seasonal averages, the real indicators to monitor in 2026 include:

- Rainfall distribution in July–August

- Mid-season reservoir levels

- Trends in vegetable and edible oil prices

- Government buffer and trade actions

- RBI’s evolving inflation assessment

These variables will determine whether a weaker monsoon remains a manageable adjustment or evolves into a more persistent macro challenge.

Bottom Line: A Manageable Risk, Not a Foregone Crisis

Early forecasts suggest Monsoon 2026 may be below normal, with risks concentrated in the latter half of the season due to rising El Niño probabilities. However, India is structurally better positioned than in the past.

The monsoon should be viewed as a macro risk to monitor—not a crisis to fear. Outcomes will depend far more on distribution, persistence and policy response than on the headline rainfall number.

Shibani Kurian, Senior Executive Vice President, Fund Manager & Head – Equity Research, Kotak Mahindra Asset Management Co. Ltd says, “On one hand, a possibly weaker monsoons could reintroduce a mild macro headwind for India. On the other, its overall impact on the Indian economy and corporate earnings is increasingly moderated by several structural buffers. Over the past decade, expanded irrigation coverage, improved reservoir levels, and better crop management have reduced the direct dependence on rainfall. Moreover, the actual impact of monsoon depends not just on the quantum but the spatial and temporal distribution of the same. At the macro level, India’s diversified growth drivers also limit the systemic of monsoons impact relative to earlier cycles. “

KMAMC is not guaranteeing/offering/communicating any indicative yield/returns on investments. The stocks/sectors mentioned in this slide do not constitute any recommendation and Kotak Mahindra Mutual Fund may or may not have any future position in these sectors/stocks.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

SEBI Registered Name - Kotak Mahindra Mutual Fund

SEBI Registered Number - MF/038/98/1