25 Mar 2026

The private credit market, loosely defined as loans made to companies by non-bank institutions has grown significantly in the past decade especially in the developed markets like USA.

Unlike traditional bank loans, these solutions are flexible and can be structured to suit the borrower’s specific needs in terms of size, type, and timing. Most private credit investments are floating rate, meaning returns adjust with interest rates and may offer better protection than fixed rate bonds.

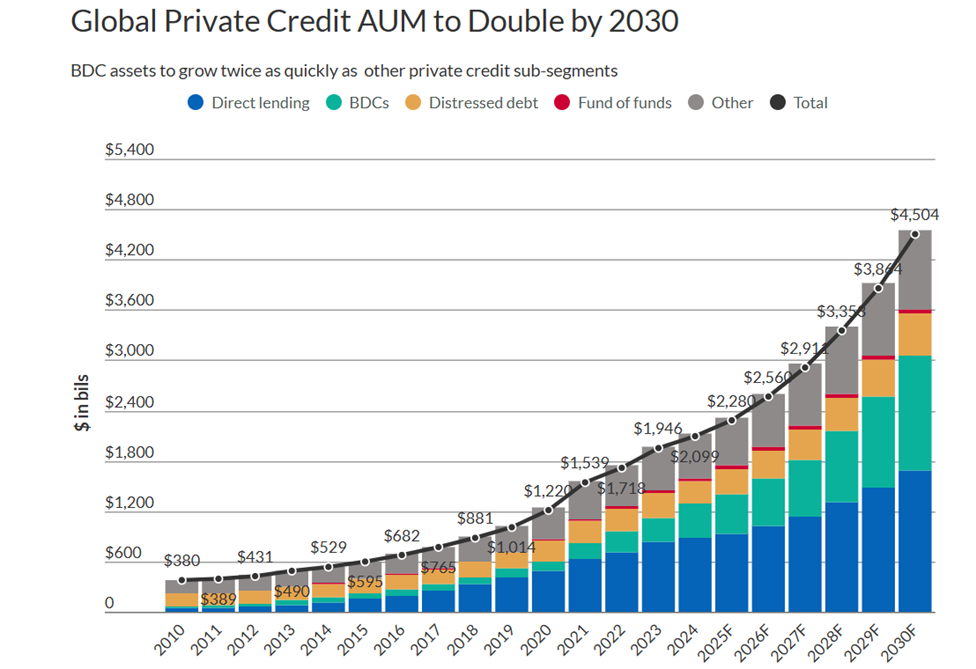

Once a niche sector, private credit filled the gap left by traditional banks tightening their lending after the 2008 financial crisis with assets under management (AUM) soaring from roughly $44 billion in 2000 to more than $2 trillion at present, this growth has largely been seen in US market, private credit stands as a major force in global finance. Growth has also been driven by market volatility and tighter bank regulations, pushing borrowers toward faster execution and greater price certainty.

Source: UBS Asset management, 22 April 2024 | https://www.kitco.com/news/article/2026-03-11/private-credit-risks-could-trigger-prolonged-economic-downturn-supports, As per latest available data

Notes: Private credit forecasts are from Preqin. "Other" includes mezzanine financing, special solutions, multi-asset special solutions, and venture debt. To avoid double-counting, the total column excludes fund of funds. Total includes BDCs (Business Development Company) but excludes all other semi-liquid funds.

Source: Fitch Ratings article as on 25th Dec 2025, Preqin, as per latest data available

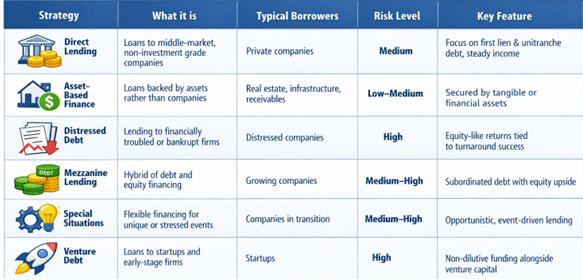

As the market expanded rapidly, it also diversified across borrower types, loan structures and collateral profiles. Private Credit is generally made up of six sub-strategies. These sub-strategies are categorized either by the types of borrowers they lend to (e.g., Distressed or Venture strategies), the types of loans they make (e.g., Direct Lending or Mezzanine), or the collateral type (e.g., Asset-Based). Each strategy offers a trade-off of risk/reward characteristics.

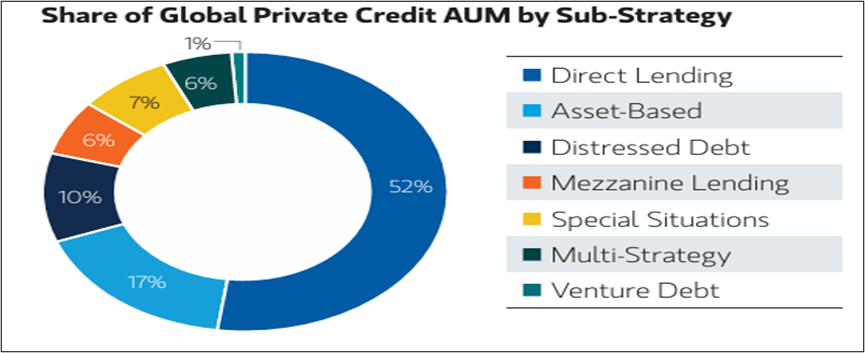

Source: PitchBook, LSEG (London Stock Exchange Group), Morgan Stanley Investment Management. Gross invested assets inclusive of leverage applied. Excludes uncalled capital in drawdown funds. As of September 30, 2025, As per latest data available.

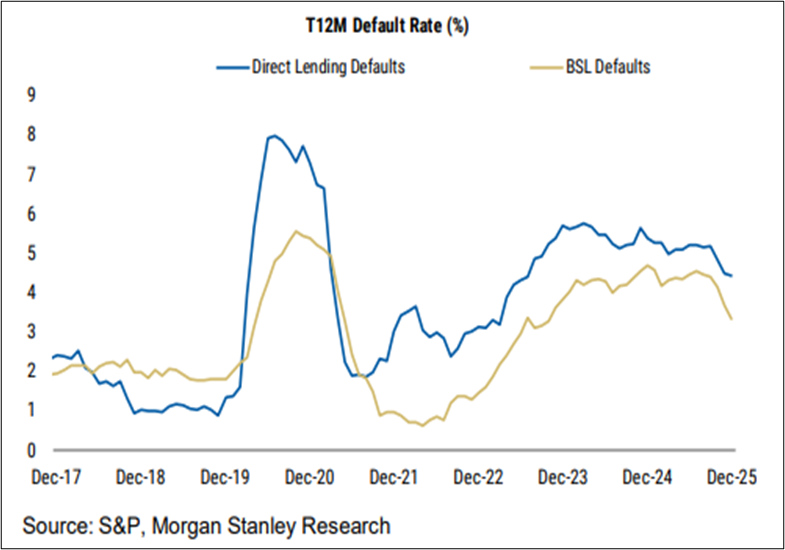

This growth has brought clear benefits: Borrowers in need, often middle-market firms in sectors like technology, healthcare, real estate and private equity buyouts obtained funding that might not have been available from banks, which are generally cautious and have regulatory restrictions. Investors may have enjoyed strong returns from higher interest rates and “illiquidity premiums” (extra yield for tying up funds long-term). For much of the past decade, default rates in private credit remained low, reinforcing confidence in the asset class.

The growth has been seen largely in USA market. These benefits were largely a function of a benign macro environment. But as the market expands rapidly and credit conditions tighten globally, questions / concerns are now emerging around credit quality and liquidity. As interest rates rose sharply, the very features that fuelled private credit’s growth began to expose underlying vulnerabilities. Higher interest costs have squeezed corporate borrowers that loaded up on floating-rate private loans during the easy-money era. Borrowers’ interest payments have doubled or even tripled in some cases, straining highly leveraged firms.

Source: https://www.hedgeco.net/news/03/2026/jamie-dimon-and-boaz-weinsteins-40-trillion-private-credit-warning.html, As per latest data available

Compounding refinancing stress, earnings visibility for a large subset of private credit borrowers has weakened. JPMorgan Chase has marked down certain exposures, particularly in software-linked loans, signalling a more cautious lending stance.

Concerns around valuations, transparency, and exposure to troubled borrowers have weighed on sentiment, particularly after defaults by private credit subprime auto lender Tricolor and auto-parts maker First Brands Group.

These structural pressures are now showing up not just at the borrower level, but at the fund level. Credit conditions tightened further. Blue Owl Capital, a major direct lending firm, halted regular quarterly withdrawals from one of its $1.6 billion funds. Blue Owl also sold over $1.4 billion of loans to raise cash, underscoring the liquidity strain in the sector.

In the first quarter alone, investors sought to withdraw billions from major private credit funds. BlackRock’s HPS Corporate Lending Fund received redemption requests of about $1.2 billion, or 9.3% of assets, but capped payouts at 5%, returning roughly $620 million. Morgan Stanley’s North Haven Private Income Fund faced requests nearing 11% of its assets and paid out only about $169 million, less than half the demand.

At Blackstone, BCRED (Blackstone Private Credit Fund) saw withdrawal requests of around $3.7 billion. The firm raised its redemption limit to 7% and deployed $400 million of internal capital to meet investor exits. Meanwhile, Cliff water capped redemptions at 7% after investors attempted to pull about 14% of capital.

What ties these episodes together is a structural liquidity mismatch. These funds lend through long-term, illiquid loans while still offering periodic withdrawals, and when too many investors try to exit at the same time, managers are forced to restrict withdrawals to avoid losses, as seen with firms like BlackRock and Morgan Stanley.

In USA market, beyond cyclical pressure, private credit is also facing a structural earnings challenge. Default rates have started to rise with Morgan Stanley expecting them to hit 8% as AI-Disruption Unfolds. Around 25 to 40 % of private credit exposure is to software and tech companies, and AI is now increasing competition and putting pressure on margins, with early stress already visible as $17.7 billion of tech loans turned distressed in a short span, ultimately pushing investors to question whether these borrowers can continue to generate stable and predictable earnings.

Source: reuters.com article dated 16th March 2026, investing.com, Bloomberg article dated 4th Feb 2026, Business insider, As per latest data available

It’s worth noting that private credit has not (yet) caused a full-blown financial crisis, and there are arguments that it might not, due to its smaller size relative to the overall financial system and structural features. For example, at < 1% of global securities markets, private credit is still much less pervasive than the subprime mortgage market was in 2007.

Source: https://www.hedgeco.net/news/03/2026/jamie-dimon-and-boaz-weinsteins-40-trillion-private-credit-warning.html

Taken together, developments in private credit point to an asset class that is being tested for the first time by a sustained period of higher rates, weaker earnings visibility, and tightening liquidity in the USA market. The risks are real, but uneven and shaped as much by fund structure, borrower profile, and regulatory design as by the broader macro environment. Outcomes are therefore likely to diverge sharply across markets and vehicles, rather than unfold as a single uniform crisis.

Shifting focus to India, the private credit market operates in a fundamentally different structural and regulatory context.

India Is still Structurally a Lower-Leverage Economy: India's corporate credit-to-GDP remained flat at 57% between 2013 and 2023, even as the economy grew substantially. Private credit in India accounts for roughly 0.6% of GDP today, with AUM of approximately $25–30 billion - representing barely 1% of total bank credit. On a relative penetration basis, India's private credit market is at approximately one-tenth of where the US stands. This underscores that private credit in India is still at an early stage of penetration rather than a mature, crowded segment. Additionally, the Debt Market Infrastructure in India is currently pretty nascent.

Source: Ascertis Credit, As per latest data available

Private credit plays a complementary role in India: In the US, private credit grew partly by taking market share from banks and syndicated loan markets (Fed Boston, May 2025; IMF GFSR (Global Financial Stability Report) April 2024). In India, private credit serves end-uses that banks may structurally underserve - acquisition financing, incremental capex funding, refinancing, promoter financing, and complex structured transactions. It also plays a role in mobilising sophisticated investment capital into a new asset class, improving capital allocation, and diversifying investor portfolios beyond equities and real estate. In doing so, it helps mitigate the risk of asset bubbles in concentrated markets and builds depth in India's evolving credit ecosystem. Private credit in India is not taking share from banks — it is addressing specific financing gaps.

Perhaps the most important structural safeguard:

Private credit in India operates primarily through SEBI-regulated Category II AIFs - closed-ended structures targeting only sophisticated investors, with prescribed disclosure requirements, valuation norms, and critically, restrictions on fund-level leverage. Category I and Category II AIFs are prohibited from taking long-term leverage meaning any loss from their lending or investment exposures does not cascade into the wider financial system. There are no semi-liquid retail vehicles, no BDC-equivalent structures democratising access to unsophisticated investors, and no quarterly redemption promises that create liquidity mismatches.

India's banking system also has negligible exposure to private credit AIFs. The RBI has proactively ring‑fenced bank exposure to AIFs, and lending to private credit providers remains tightly regulated (Moody’s, 2025). As a result, the interconnectedness between banks, insurers, and private credit funds, a key regulatory concern in several developed markets, remains limited in India.

The very issues at the heart of the Blue Owl episode - retail investor exposure, liquidity-maturity mismatches, opaque valuations, and semi-liquid structures that promise liquidity they cannot deliver - simply do not apply to the Indian market.

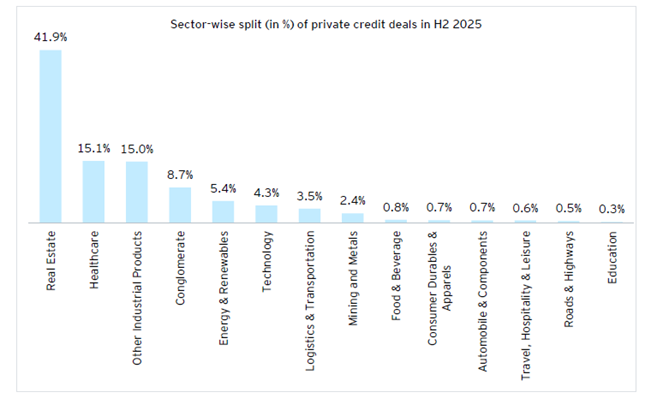

The Indian private credit funding has been primarily used for real assets creation. As per EY report, the below is sector wise split (in %) of Private Credit Deals in India in H2 2025

Source: EY Report – Private Credit in India H2 2025 update

Taken together, the recent stress in private credit in US markets highlights that outcomes are ultimately shaped by structure rather than the asset class itself. While the US market is grappling with liquidity mismatches, opaque valuations, and retail investor exposure, India’s private credit ecosystem is built very differently — with closed‑ended funds, strict leverage limits, limited bank interconnectedness, and access restricted to sophisticated investors. These structural safeguards materially reduce the risk of sudden, disorderly outcomes. As a result, even as private credit globally enters a more testing phase, India remains structurally positioned to possibly grow further.

Sunit Garg, CIO – AIF, Kotak Mahindra Asset Management Company states, “As can be seen from the above, structurally the USA and Indian private credit markets are very different. Indian private credit market is at nascent stage of growth and poised to grow multi fold in the coming years. There are various regulatory safeguards to Indian private credit market such as, no long term leverage at fund level, close ended nature of most of the funds, hence, no liquidity / asset liability mismatch issue, investment by only sophisticated investors, no major inter-connectedness with other financial markets such as banks etc. Further, the lending from Indian private credit markets have largely been for real assets.

From Indian investor perspective, private credit should be seen as one of the core allocations which provides a relatively stable return.”

Srini Sriniwasan, Managing Director, Kotak Alternate Asset Managers Limited states, “There’s a fair amount of noise around redemptions and gating in a number of global private credit funds. The issues unfolding in the US have less to do with private credit as an idea and everything to do with how certain funds were built. The stress in global private credit markets stems largely from liquidity mismatches. India simply does not operate under that model. Many private credit funds here are closed‑ended. Investors commit money to the entire life of the fund. Additionally, most of our Private and High Yield credit strategies are senior secured positions unlike some other markets. Regulations do not permit leverage at fund level which restricts contagion risk to system as well. Overall credit requirements in an economy which is growing is much larger than available resources. The demand is structural, not speculative. So, when comparisons are made between India and the US, I return to what the facts show. India’s private credit market is structured differently, governed responsibly, and supported by real economic demand and those facts are reassuring.”

The stocks/sectors mentioned do not constitute any kind of recommendation and are for information purpose only. Kotak Mahindra Mutual Fund may or may not hold position in the mentioned stock(s)/sector(s). These materials are not intended for distribution to or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. The distribution of this document in certain jurisdictions may be restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions. Use of the company/ brand names does not imply any affiliation with or endorsement by them or any of its holding companies, subsidiaries or affiliates and are used for illustrative purpose only.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.