20 Apr 2026

The global oil and gas industry is once again at the centre of attention. Geopolitical tensions, supply disruptions and evolving energy markets have combined to create an environment best described as “shifting sands” i.e. constantly evolving and unpredictable.

Historically, oil markets have witnessed multiple disruptions, from the Suez Crisis in the 1950s to the Gulf War and the Russia‑Ukraine conflict. What makes the current situation stand out is the scale of disruption combined with very low spare capacity.

Nearly 20% of global oil supply is affected, while spare capacity has fallen to around 3%, compared to over 30% during earlier crises. This imbalance has placed global energy markets under severe stress, amplifying volatility and uncertainty.

| Crisis | Timeline | Global Demand (mn bpd) | Supply Disrupted (%) | Spare Capacity Available (%) |

|---|---|---|---|---|

| Suez Crisis | 1956-57 | NA | 10 | 35 |

| Arab Oil Embargo | 1973 | 56 | 7 | 8 |

| Iran Revolution | 1978-79 | 64 | 5 | 5 |

| Gulf War | 1990-91 | 67 | 9 | 4 |

| Russia-Ukraine War | 2022-? | 98 | 2 | 5 |

| Iran War | 2026-? | 101 | 20 | 3 |

Source: CNBC, Raidan Energy, BP Statistical Review of World Energy, Kotak Institutional Equity, Kotak Mahindra AMC, mn bpd- Million barrels per day

At the heart of the crisis is the Strait of Hormuz, one of the world’s most critical energy chokepoints:

- ~20% of global oil production passes through it

- ~27% of global maritime oil trade

- ~20% of global LNG trade

- ~40% of India’s crude oil imports

- ~55% of India’s LNG imports

Source: Bloomberg, US EIA, Kotak Institutional equities, As per latest data available

Disruptions here have dramatically reduced tanker movement, blocking millions of barrels of oil and significant LNG volumes on a daily basis. Crude oil markets have shown unusual price distortions. While global benchmarks like Brent and WTI (West Texas Intermediate) typically move closely, the WTI which originates from North America was trading at a discount to the Brent. This is because the crude from countries like Oman, Dubai, etc has not been free flowing since the onset of the war.

Benchmark refining margins across regions are also showing divergent trends and levels. However, this is due to methodology for calculation which differs. E.g. Dubai crude is used to calculate Singapore Complex margin but due to high price of Dubai, margins appear negative.

In reality, refining margins for refineries are strong due to product market being tighter due to disruption. However, quotes for products could be different from actual refinery transfer prices in the current scenario.

While the immediate crisis centres on the vulnerability of critical maritime routes like the Strait of Hormuz, it is worth noting that India's oil and gas consumption together account for approximately 25–30% of the nation's total energy demand, underscoring their significant role in India's overall energy mix.

However, India’s vulnerability lies not in consumption share, but in import dependence. With only about 13% of crude oil needs met domestically, India remains highly sensitive to global price movements and supply disruptions.

Source: BP Statistical Review 2025, Kotak Mahindra AMC, As per latest data available

India’s strategic oil reserves cover roughly 30 days, with only 8–9 days in government‑owned strategic reserves. While this is lower than peers like Japan or Korea, India has managed near‑term pressures by diversifying crude sourcing most notably through higher crude oil imports from Russia and the United States, alongside traditional Middle Eastern suppliers.

Source: JP Morgan report dated 22/03/2026, Assessed on 16 March 2026, As per latest data available

This flexibility is also reflected in India’s petroleum products balance. During Apr-Feb’26, India produced ~257 million tonnes of petroleum products while domestic consumption stood at ~222 million tonnes, making India a net exporter of ~43 million tonnes. Diesel and petrol, together accounting for over 60% of total production, remain net export products providing resilience during crude supply disruptions.

However, LPG stands out as a clear exception. LPG production was only ~12 million tonnes, while consumption reached ~31 million tonnes, resulting in net imports of ~20 million tonnes. This makes LPG structurally vulnerable despite India’s overall strength in refining and product exports.

Source: PPAC, Kotak Mahindra AMC, as of Feb 2026

When the discussion shifts from oil to gas, it is important to highlight how the challenges differ from those in the oil sector. While oil markets are experiencing distortions and some flexibility due to alternative sourcing, the gas market, especially LNG is facing deeper, more structural issues.

It is crucial to emphasise that natural gas, particularly in the form of LNG, is much less flexible than oil because of its storage and transportation constraints. Disruptions at major supply hubs like Qatar’s Ras Laffan LNG complex have led to significant shortages, causing Asian and European LNG prices to surge sharply even during typically low-demand periods. This makes the gas crisis more persistent and difficult to resolve, compared to the oil market, where alternative suppliers can be tapped more readily.

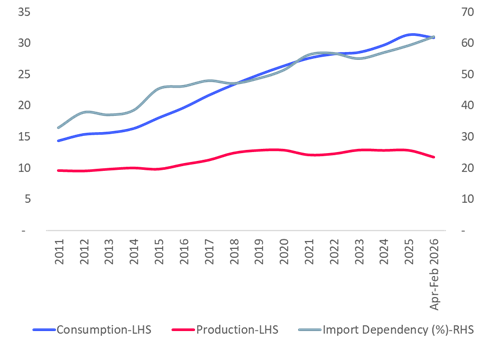

Moreover, LPG consumption has risen steadily over time, while domestic production has remained broadly flat, pushing import dependency above 60%.

India LPG demand-supply For Fiscal YE March

Source: PPAC, Kotak Institutional Equities, Kotak Mahindra AMC

In summary, when discussing gas, focus on the heightened vulnerability due to supply bottlenecks, limited storage options and the resulting price volatility. These factors collectively make gas shortages more enduring and challenging than those seen in the oil sector.

Government Response: Shielding the Consumer

To limit inflationary shock, the Government of India has taken multiple steps:

- ₹10 per litre cut in excise duty on petrol and diesel

- Reintroduction of windfall tax on fuel exports

- Prioritisation of gas supply to CNG and domestic PNG

Source: MOPNG, MOF, Kotak Institutional Equities, Kotak Mahindra AMC, As per latest data available

While these measures strain the fiscal position, they help protect households and essential transport from immediate price spikes. The burden is largely absorbed by oil marketing companies, with policy support expected to evolve if the crisis persists.

The current oil and gas crisis remains fluid, with outcomes dependent on geopolitical developments and supply restoration timelines. While oil prices may eventually stabilise in a higher‑for‑longer range due to risk premiums, gas markets could remain tight for longer.

Over the long term, this episode is likely to accelerate:

- Energy diversification

- Renewable adoption

- Policy focus on supply security

For investors, the message is clear: don’t react, stay disciplined and keep sight of long‑term goals.

Periods of geopolitical turmoil often trigger sharp market corrections driven by fear and headlines. History suggests, however, that markets tend to recover once uncertainty begins to ease, often before news flow improves.

Key investor takeaways:

- Short‑term volatility is unavoidable and news‑driven

- Long‑term market direction depends on fundamentals, not headlines

- Staggered investments help manage timing risk

- Asset allocation discipline matters more than tips

Whether it was COVID‑19, the Russia‑Ukraine conflict or earlier wars, markets have rewarded investors who stayed invested through periods of uncertainty.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

These materials are not intended for distribution to or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. The distribution of this document in certain jurisdictions may be restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions. The stocks/sectors mentioned do not constitute any kind of recommendation and are for information purpose only. Kotak Mahindra Mutual Fund may or may not hold position in the mentioned stock(s)/sector(s).