25 Feb 2026

Did you know that?

In 2025, stablecoins quietly rewrote the rules of global money movement. They processed an astonishing $33 trillion worth of transactions in 2025 which is more than Visa & Mastercard combined.

Source: https://www.binance.com/en-IN/square/post/35697613698841

But before we deep dive into the world of stable coins: we need to understand what exactly are stablecoins?

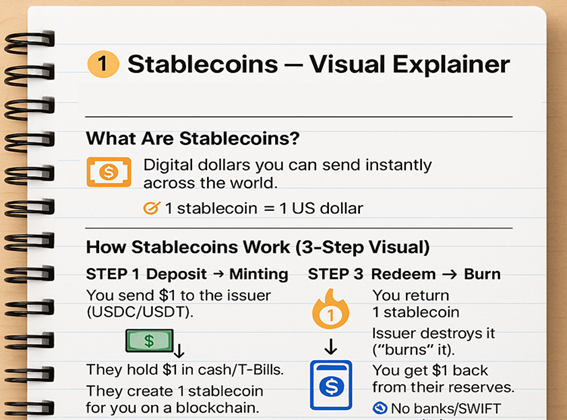

Stablecoins are cryptocurrencies designed to hold a stable value, usually pegged 1:1 to a fiat currency like the US Dollar. Think of them as a digital currency on the blockchain. Their core purpose is to solve crypto’s biggest problem: volatility. Unlike Bitcoin or Ether, which can swing 10–20% in a day, stablecoins stay near $1 and thus act as a reliable medium of exchange, settlement asset and store of value.

The stablecoin market has not just grown; it has fundamentally re-architected the plumbing of global finance. We are looking at a ~$310 billion asset class that is now processing more value than the world's largest credit card networks combined.

For decades, Visa and Mastercard have been the untouchable titans of global payments. In 2025, that era may be nearing an end. Stablecoins are now settling more value than Visa and Mastercard combined. While credit cards take 24-48 hours to settle, stablecoins like USDC (USD Coin, a U.S. dollar‑pegged stablecoin issued by Circle Internet Financial) and USDT (USD Tether, a U.S. dollar‑pegged stablecoin issued by Tether Limited) are moving billions in seconds, 24/7, without a single bank branch opening its doors.

Source: S&P Global

Source: bitcoin.com, coincentral.com, coinlaw.io & cryptonews.com, The above values are approximate.

There are 3 primary categories of stablecoins:-

| Type | Examples | Description |

|---|---|---|

| Fiat Collateralized | USDT (Tether), USDC (Circle) | Backed 1:1 by USD or cash equivalents held in reserves |

| Crypto Collateralized | DAI (MakerDAO) | Over-collateralized by other cryptocurrencies via smart contracts/protocols |

| Algorithmic | (Mostly defunct, e.g., old UST) | Algorithms automatically adjust supply and demand to maintain price stability |

The stablecoin market is highly concentrated. Almost 99% of stablecoin market capitalisation is denominated in USD, and just two issuers, Tether (USDT) and Circle (USDC), account for ~85% of total market cap.

Source: RBI Financial Stability Report

That concentration matters because stablecoins aren’t just “crypto tokens”, they are reserve portfolios wrapped in a payments interface. As stablecoins scale, issuers are pushed towards holding more U.S. Treasury bills, to maintain confidence in redemption at par. Stablecoins are now a meaningful part of short‑term dollar markets because issuers park a large share of reserves in U.S. Treasury bills. To put this in perspective: Stablecoin issuers now hold more U.S. government debt than Germany, South Korea, or UAE. Tether (USDT), the market leader with a 60.4% share, now holds approximately $141.6 billion in U.S. Treasury bills. In a stress event, such scale matters, a loss of confidence could trigger redemptions and force fire sales of reserve assets, transmitting volatility from stablecoins into traditional money markets. This makes companies like Tether not just a crypto company, but a critical pillar of the U.S. Treasury market. If Tether sneezes, the bond market may catch a cold.

Source: Binance, tether.io, Messari.io

Silicon Valley Bank’s (SVB) collapse in March 2023 exposed a key truth: USDC briefly fell below $1 after it’s issuer Circle disclosed that ~8% of reserves at SVB the failed lender, showing how a confidence shock can trigger redemptions.

Source: Financial Times, February 2, 2026

And this wasn’t happening in isolation. The market was still carrying the scars of TerraUSD’s collapse, a reminder that “stable” depends on trust, and trust can vanish overnight.

Source: corporatefinanceinstitute.com

That is why 2025 became the turning point. On July 18, 2025, President Trump signed the GENIUS (Guiding and Establishing National Innovation for U.S. Stablecoins) Act, bringing stablecoins under a formal U.S. rulebook. The Wild West phase didn’t end because things became safe; it ended because the system had already seen what happens when it isn’t. In May 2022, the industry learned a brutal lesson: Math is not money. Unlike Tether or Circle, which hold real dollars in a vault, TerraUSD (UST) was an "algorithmic" stablecoin. It relied on a dual-token system where a volatile cryptocurrency (LUNA) was burned or minted to keep the stablecoin at $1. It was a perpetual motion machine fuelled entirely by confidence. Post-mortem analysis exposed that this "decentralized" miracle was rigged. Terraform Labs had been secretly buying UST to prop up the price long before the crash. When they stopped, gravity took over. In just 6 days (May 7–13, 2022), the peg broke. Despite deploying $1.5 billion in Bitcoin reserves to defend it, the system collapsed. The Cost: $40 billion in value evaporated instantly. It wiped out life savings and toppled major lenders like Celsius, creating the "trust deficit" that defined the next three years.

Source: CNBC, Yahoo finance

The GENIUS Act put stablecoins on a tighter leash. It requires “payment stablecoins” to be fully backed 1:1 with high quality liquid assets like cash, insured deposits, and short dated U.S. Treasuries and it pushes issuers to disclose reserve composition regularly. In practice, this framework shuts the door on “algorithmic” designs for regulated payment use: if a coin can’t maintain 1:1 reserve backing, it doesn’t qualify under the Act’s definition and requirements

Source: Circle Transparency Reports.

Most importantly, GENIUS creates the first federal rulebook and approval pathway for stablecoin issuers moving stablecoins from a loosely governed market into the perimeter of the U.S. financial system.

Despite the regulation, "stable" does not mean "risk-free." Just four months ago, on October 10, 2025, the market witnessed a ~$19 billion liquidation cascade.

Ethena’s USDe (a synthetic dollar) briefly traded down to ~$0.65 on Binance after an exchange side oracle/pricing issue misread its price during thin liquidity. This pricing error triggered automated liquidation engines, causing massive losses despite the asset theoretically remaining stable. This proves that even with robust collateral, the infrastructure (oracles, exchanges) remains a critical point of failure.

Source: Binance, bitcoin.com

Despite all this, it helps to ask a basic question: what are stablecoins used for? They function primarily as money, not investments, as they do not pay interest and are restricted from doing so under the GENIUS Act.

Once you start treating stablecoins as payment, the use cases fall into place. The market isn’t adopting stablecoins because people want another thing to speculate on; it’s adopting them because certain money flows (especially in and around crypto) need a fast, always on, dollar-like settlement layer.

Stablecoins already function as the working cash balance of crypto markets. Traders need a stable unit to park value, post collateral, and move between positions without constantly re-entering the banking system. That is why stablecoins account for a dominant share of exchange activity: over 80% of trading volume on major centralised crypto exchanges, essentially acting as the settlement asset for crypto trading and liquidity provision.

Source: RBI FSR

Stablecoins have also become the preferred rail for illicit crypto flows. Since 2022, stablecoins have replaced Bitcoin as the primary vehicle for illicit activity on-chain, largely because they combine speed, liquidity and relative price stability. According to crypto research firm Chainalysis, stablecoins have "dominated" illicit money movements, accounting for 84% of all illicit transaction volume globally last year. Tether (USDT), in particular, is frequently cited in international investigations. It has become the preferred vehicle for sanctions evasion and moving value without a trace.

For cross-border payments, stablecoins are much faster than traditional SWIFT (Society for Worldwide Interbank Financial Telecommunication, a global messaging network used by banks and financial institutions for cross‑border payments.) transfers. While a bank wire costs $15-$50, a stablecoin transfer on networks like Solana or Tron costs less than $0.01. In Latin America, 71% of stablecoin activity is already tied to remittances and inflation hedging, bypassing local banking failures entirely.

Source: wise.com, Razorpay, RebelFI

Another important use case is not “payments innovation” but “currency preference.” Stablecoins can provide a more convenient way to hold and transfer dollar value in countries where inflation is high or trust in the local system is low.

Stablecoins don’t just change how money moves, they can change how money behaves in the economy. If dollar stablecoins become a widely accepted cash substitute, they can effectively expand the pool of dollar-like spending power; even if they’re treated as a separate asset, they can still matter by reducing demand for traditional fiat money. Either way, the gap between money supply and money demand is what drives prices and real yields which is why stablecoin growth can become macro-relevant.

That’s why even central bankers have begun talking about stablecoins as macro infrastructure.

For instance, the Bank of Korea Governor Rhee Chang-yong revealed South Korea is considering a new registration regime for domestic virtual asset issuance, while warning that won-denominated stablecoins could enable capital flow circumvention. China has also banned stablecoins as they threaten exchange rate management and capital controls, while experimenting cautiously through Hong Kong.

Overall, currently stablecoins create structural demand for U.S. government debt because reserves are largely held in short term Treasuries and similar instruments. U.S. policymakers see this as a feature, Treasury Secretary Scott Bessent has suggested the stablecoin market could grow toward $2 trillion, potentially creating a large new buyer base for Treasuries and reinforcing global dollar usage.

Source: Bloomberg

Stablecoins are quickly becoming a USD‑denominated settlement layer built on liquid reserves. Yet the system remains vulnerable: a loss of confidence can spark sudden redemptions, push issuers into selling their reserves, and spill volatility into traditional money markets. Regulations help contain the risk, but they can’t fully remove it.

Paolo Ardoino, CEO, Tether: “The stablecoins that last are the ones built around the real needs of their users, not around flash or hype. That means being reliable in everyday conditions, transparent about reserves, and consistent over time. Trust is earned by meeting those expectations day after day, not by chasing headlines.”

Kash Razzaghi, Chief Commercial Officer, Circle: “Stablecoins are rewriting how value moves through financial systems. The business case is clear: faster settlement, fewer intermediaries, and tighter treasury control are driving enterprise and institutional adoption of assets such as USDC.”

Source: The 2026 Stablecoin Momentum Report by Zerohash

Sudheer Guntupalli, Vice President, Equity Research at Kotak AMC, adds: “The global economy is currently undergoing a massive re-plumbing, attempting to marry the frictionless velocity of the internet with the heavy, regulated gravity of sovereign fiat. Stablecoins have emerged as the ‘bridge to somewhere’, finally allowing capital to move as fast as a viral meme on social media. By eliminating the ‘settlement holiday’, they liberate billions from the purgatory of three day bank transfers. However, this high speed efficiency is not a free lunch. The ‘stability’ in their name is only as robust as the transparency of their reserves and the strength of the digital pipes they travel through. In 2026, the real economic question isn’t just about speed, but whether we are trading the slow moving frustrations of legacy banking for the instantaneous, systemic risks of a 24/7 digital ledger. They are the silent engine of modern trade – efficient, yes. But, only as reliable as the code and collateral backing them.”

KMAMC is not guaranteeing/offering/communicating any indicative yield/returns on investments. The stocks/sectors mentioned do not constitute any kind of recommendation and are for information purpose only. Kotak Mahindra Mutual Fund may or may not hold position in the mentioned stock(s)/sector(s). Companies mentioned don’t constitute recommendation, brand name affiliation disclaimer & companies mentioned for illustrative purpose only. These materials are not intended for distribution to or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. The distribution of this document in certain jurisdictions may be restricted or totally prohibited and accordingly, persons who come into possession of this document are required to inform themselves about, and to observe, any such restrictions.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.