29 Aug 2025

Investing in mutual funds is a powerful way to grow wealth but understanding how your returns are taxed is essential. Based on the period of holding, mutual fund returns are categorised into short term capital gains and long term capital gains. The concept of "short term vs long term capital gains" is crucial for investors to understand. By holding investments for the long term, you can reduce the amount of taxes owed, allowing you to keep more of your gains. This tax advantage makes long-term investing an effective strategy for accumulating wealth. Understanding these tax distinctions can help you make better decisions about when to buy and sell your mutual funds.

Key Takeaways

- Short Term vs Long Term Capital Gains: Short term gains (held ≤ 1 year in case of certain securities and units) are taxed at a higher rate (20% for equity oriented mutual fund units), while long term gains (held > 1 year) are taxed at a lower rate (12.5% for equity oriented mutual fund units) with a ₹1.25 lakh exemption.

- Tax Efficiency: Long term investing offers tax benefits and better growth potential due to lower tax rates.

- SIP and Tax Benefits: Investing through SIP, especially in ELSS funds, can provide tax benefits through SIP and deductions under Section 80C, saving up to ₹1.5 lakh on taxable income (Old Regime).

- Effective Tax Planning: Understanding short term vs long term capital gains helps reduce taxes and maximize returns.

- Investing in ELSS: ELSS funds offer both tax savings (Old Regime) and long term growth potential when invested via SIPs.

What is Tax on Mutual Funds?

Returns earned through mutual fund investments are classified as capital gains and are taxed based on how long you hold the investment.

The distinction based on the period of holding plays a crucial role in Mutual Fund Taxation:

- Short term capital gains (STCG) are typically taxed at a higher rate.

- Long term capital gains (LTCG) enjoy a lower tax rate, making long term investing more tax efficient.

Understanding the difference between short term vs long term capital gains helps you make smarter investment decisions, minimize tax liability, and maximize overall returns. Timing your exits wisely can lead to more efficient wealth growth, particularly if you understand how to optimize capital gain.

Understanding Capital Gains

When investors redeem mutual fund units at a price higher than the purchase cost, the profit earned is referred to as a capital gain. These gains are subject to tax, but the rate and classification depend on two factors:

- The nature of the underlying asset held by the mutual fund (such as equity or debt), and

- The holding period, i.e., the duration for which the units were held before redemption.

Based on these factors, capital gains are broadly categorised into short term and long term. Each category is taxed differently as per prevailing tax regulations. Equity oriented funds and debt oriented funds follow different rules for determining the classification and taxation of gains.

Understanding this distinction is essential for investors to plan their redemptions effectively. A clear grasp of how asset type and holding period influence tax treatment can help optimise after tax returns and support more informed investment decisions.

Understanding the difference between short term vs long term capital gains is essential for effective tax planning.

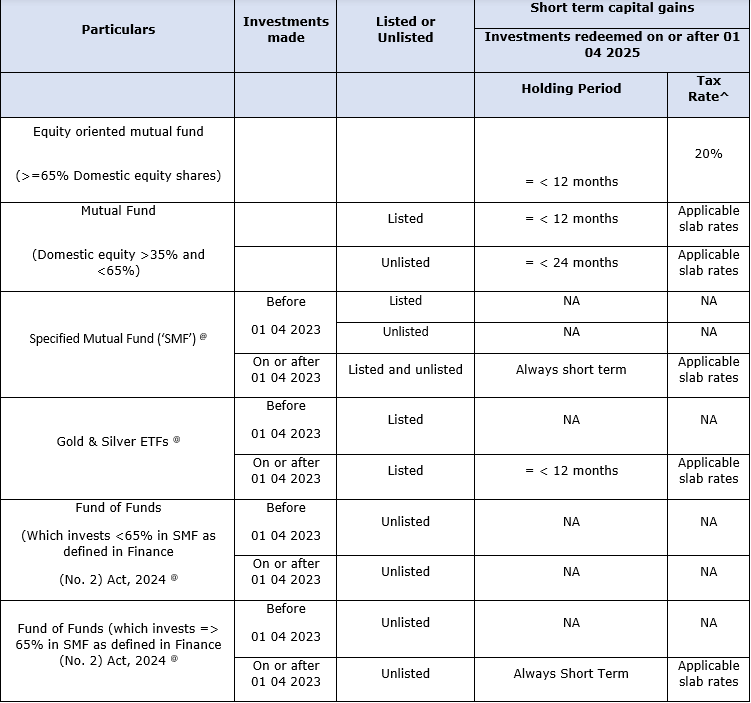

What are Short Term Capital Gains?

Short Term Capital Gains (STCG) refer to the profits earned when you sell your mutual fund units within a short period after purchasing them. The definition of “short term” depends on the type of fund. These gains are usually taxed at higher rates than long term capital gains. Understanding how STCG works is important for planning your investments wisely and reducing your tax liability. The timing of selling your mutual fund units plays a crucial role in determining how much tax you ultimately pay on your returns.

$ Subject to NRI having Permanent Account Number (PAN) in India. The TDS deductible in case of NRI shall also be increased by applicable surcharge as per Note 1 and 4% health and education cess. In case of NRI, if PAN is not available and specified declaration is not provided as specified under Rule 37BC, TDS @ higher of 20% or rates calculated as above will be deducted. The tax rates are subject to DTAA benefits available to NRI's. As per the Finance Act 2013, submission of tax residency certificate (“TRC”) will be necessary for granting Double Taxation Avoidance Agreement (“DTAA”) benefits to non residents. A Taxpayer claiming DTAA benefit shall furnish a TRC of his residence obtained by him from the Government of that country or specified territory. Further, in addition to the TRC, the non resident shall also provide electronically filed Form 10F and such other documents /information, as may be prescribed by the Indian Tax Authorities and Kotak Mahindra Mutual Fund or Kotak Mahindra Asset Management Company Ltd. Further investor needs to certify in its No PE declaration that one of the principle purposes of investment is not to avail the treaty benefits & the investment asset & investment income are beneficially held by the investor claiming DTAA benefits.@ For FY 2024 25, Specified Mutual Fund is defined as where not more than thirty five per cent of its total proceeds is invested in the equity shares of domestic companies. However, Finance (No 2) Act, 2024 has amended the definition of Specified Mutual Fund w.e.f. FY 2025 26 as a Mutual Fund by whatever name called, which invests more than sixty five per cent of its total proceeds in debt and money market instruments; or a fund which invests sixty five per cent or more of its total proceeds in units of a fund mentioned in clause (i) ^ Tax rates for resident and non residents shall be increased by applicable surcharge as per Note 1 and 4% Health & Education Cess.

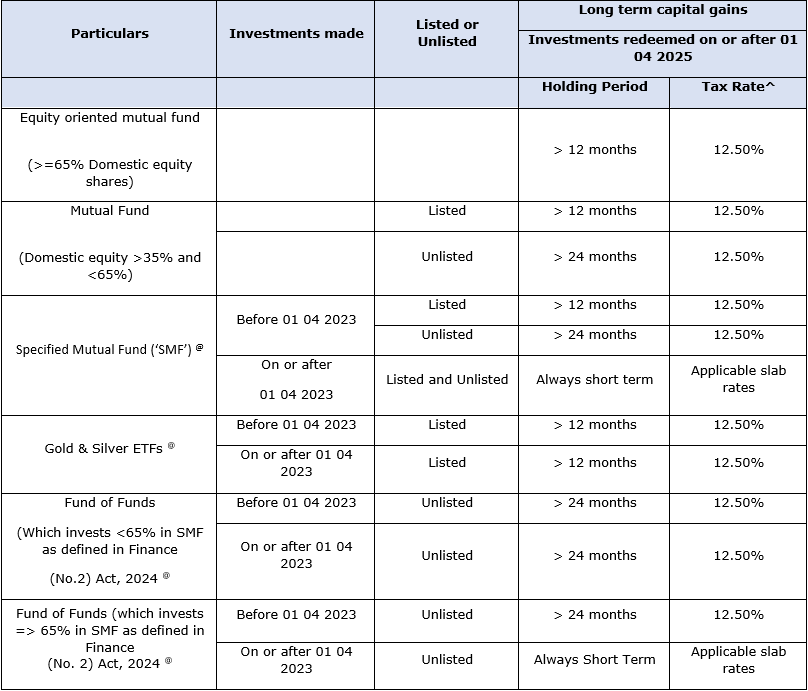

What are Long Term Capital Gains?

Long Term Capital Gains (LTCG) are the profits earned when you sell your mutual fund units after holding them for a longer period. The required holding period to qualify as long term depends on the type of mutual fund. These gains are taxed at a lower rate than short term gains, encouraging long term investing.

$ The TDS deductible in case of NRI shall also be increased by applicable surcharge as per Note 1 and 4% health and education cess. In case of NRI, if PAN is not available and specified declaration is not provided as specified under Rule 37BC, TDS @ higher of 20% or rates calculated as above will be deducted. The tax rates are subject to DTAA benefits available to NRI's. As per the Finance Act 2013, submission of tax residency certificate (“TRC”) will be necessary for granting Double Taxation Avoidance Agreement (“DTAA”) benefits to non residents. A Taxpayer claiming DTAA benefit shall furnish a TRC of his residence obtained by him from the Government of that country or specified territory. Further, in addition to the TRC, the non resident shall also provide electronically filed Form 10F and such other documents /information, as may be prescribed by the Indian Tax Authorities and Kotak Mahindra Mutual Fund or Kotak Mahindra Asset Management Company Ltd. Further investor needs to certify in its No PE declaration that the one of the principle purpose of investment is not to avail the treaty benefits & the investment asset & investment income are beneficial hold by the investor claiming DTAA benefits.

@ For FY 2024 25, Specified Mutual Fund is defined as where not more than thirty five per cent of its total proceeds is invested in the equity shares of domestic companies. However, Finance (No 2) Bill, 2024 has amended the definition of Specified Mutual Fund w.e.f. FY 2025 26 as a Mutual Fund by whatever name called, which invests more than sixty five per cent of its total proceeds in debt and money market instruments;or a fund which invests sixty five per cent or more of its total proceeds in units of a fund mentioned in clause (i) ^ Tax rates for resident and non residents shall be increased by applicable surcharge and health and education cess. The salient features of the capital gain tax are as under:

Any transfer of equity-oriented fund units on or after 1 April 2018, shall not be exempt under section 10(38) Long term capital gains in excess of Rs. 1.25 lakh shall be taxable at rates mentioned in table above plus surcharge (if any, as applicable) plus health & education cess @ 4%.The capital gain will be computed without giving effect to the 1st and 2nd proviso to section 48 in the manner laid down under the section i.e. without indexation benefit and without foreign currency conversion benefit. Cost for units acquired prior to 1 Feb 2018 and sold on or after 1 April 2018 will be computed as under:

Higher of: Cost of acquisition or Lower of: FMV of asset on 31 Jan 2018 Full value of consideration accruing as a result of transfer.

Latest Updates from Budget 2024 and Budget 2025

The Union Budget 2024 introduced several key changes in mutual fund taxation:

For FY 2024 25 onwards:

- LTCG on equity oriented mutual fund units revised to 12.5% from 10%

- STCG on equity oriented mutual fund units increased to 20% from 15%.

- Enhancement in the annual exemption limit from ₹1 lakh to ₹1.25 lakh for long term capital gain in case of certain capital assets including equity oriented mutual fund units

Key Difference Between Short Term and Long Term Capital Gains

|

Particulars |

Short Term Capital Gains (STCG) |

Long Term Capital Gains (LTCG) |

|

Meaning |

Gains from selling mutual fund units within the specified short holding period |

Gains from selling mutual fund units after the specified holding period |

|

Equity Mutual Funds |

Sold within 12 months |

Sold after 12 months |

|

Tax Rate (Equity Funds) |

20% (previously 15%) |

12.5% (previously 10%), with ₹1.25 lakh exemption |

|

Debt Mutual Funds |

Taxed as per income slab |

Taxed as per income slab (indexation benefit removed) |

|

Tax Efficiency |

Less tax efficient due to higher rates/slab taxation |

More tax efficient with lower flat rates |

|

Impact on Returns |

Reduces net returns if sold early |

Maximizes post tax returns if held long term |

How to Calculate Capital Gains Tax

- Classify the type of fund and holding period

- Identify gain type: short term or long term

- Apply relevant tax rate

- Deduct the exemption limit of ₹1.25 lakh if applicable (for LTCG)

Strategies to Minimize Capital Gains Taxes

Maximizing returns involves knowing how to save tax on mutual fund investments. Here are some effective strategies:

- Invest for the Long Term: Holding investments for over 12 months in case of equity oriented mutual fund schemes helps you qualify for long term capital gains (LTCG), benefiting from a lower tax rate and the ₹1.25 lakh exemption.

- Offset Short Term Losses: Use short term capital losses to offset long term capital gains, reducing taxable income.

- Invest in ELSS Funds: ELSS funds offer tax deductions under Section 80C (Old Regime), allowing you to save up to ₹1.5 lakh on taxable income. To maximize tax savings and grow wealth, investing in ELSS is a smart choice. You can avail tax benefits through SIP and long-term appreciation. Start investing and explore the benefits with the Kotak ELSS Tax Saver Fund.

Short Term vs Long Term: Which is Better

It depends on your goals:

- Need liquidity soon? STCG may suit you though taxed higher

- Building wealth? LTCG with exemption benefits is smarter

In most cases, short term vs long term capital gains should be evaluated before any redemption.

Common Misconceptions about Capital Gains

- "LTCG is always better" – Not always, It depends on returns, holding period, and tax slab.

- "Capital losses can't offset gains" – False, short term capital losses can offset Long Term Capital Gains.

Avoiding these myths helps improve your understanding of short term vs long term capital gains.

Frequently Asked Questions

Q1: What is the tax rate for short term and long term capital gains?

The tax treatment of capital gains depends on the type of mutual fund (equity oriented or debt oriented) and the holding period. Generally:

- Short term capital gains (STCG) are taxed at a higher rate than long term gains.

- Long term capital gains (LTCG) on equity mutual funds may enjoy certain exemptions up to a limit, beyond which they are taxed at a specified rate.

Q2: Is short term capital gain taxable?

Yes, STCG is fully taxable without exemptions.

Q3: How much long term capital gain is tax free?

Up to ₹1.25 lakh of long term capital gain per year in case of certain capital assets including equity oriented mutual fund units.

Q4: Is long term capital gains tax always lower than short term?

Generally yes because of the variation in the tax rates for long term and short term capital gains, but recent budget changes have narrowed the difference.

Q5: Can short term capital losses offset long term capital gains?

Yes, Short Term Capital Losses can be setoff against Long Term Capital Gains, reducing taxable income.

Q6: Do dividends count as short term or long term capital gains?

No. Dividends are taxed separately, not as capital gains.

Disclaimers

Kotak ELSS Tax Saver Fund

The contents of this article/infographic are for general informational purposes only and should not be considered as professional or financial advice. The views expressed in this Article do not necessarily constitute the views of Kotak Mahindra Asset Management Company (‘KMAMC’) or its employees. The information is subject to updation, completion, and verification, and applicable laws may vary or evolve over time. This content is not intended for distribution or use in any jurisdiction where it would be unlawful or require KMAMC or its affiliates to meet any registration or licensing obligations. KMAMC, its directors, employees and the contributors shall not be responsible or liable for any damage or loss resulting from or arising due to reliance on or use of any information contained herein. Readers should conduct their own due diligence and consult a financial advisor before making any decisions. Terms and conditions of KMAMC and relevant third parties apply. KMAMC is not responsible for third-party services. This content does not constitute an offer, advice, or solicitation for any third-party products or services. KMAMC makes no warranty of any kind with respect to the completeness or accuracy of the material and articles contained in this Article. The information contained in this Article is sourced from empanelled external experts for the benefit of the customers and it does not constitute legal advice from KMAMC. Tax laws are subject to amendment from time to time. The above information is for general understanding and reference. This is not legal advice or tax advice, and users are advised to consult their tax advisors before making any decision or taking any action

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.